Zopa Review

** Zopa review updated December 24th, 2020 **

Founded in 2005, Zopa is the largest and oldest peer to peer company and one that survived the 2008 financial crisis. That is quite an achievement considering the carnage that was left in the wake of the mortgage meltdown. Zopa has 75,000+ active investors who have lent over £3 billion to borrowers.

I’ve been on and off investing through Zopa because Zopa is incredibly easy to use and offers two simple investment choices (standard and ISA) that should appeal to a wide range of peer to peer lenders. The discontinued Access and Classic accounts and the removal of the Safeguard Provision Fund is a recent negative change for those wanting the lowest possible risk levels.

My Current Investment Amount: Click here

My current annual rate of return: 4.5% (After fees but before taxes)

[table “8” not found /]* This opinion risk factors in loan types, interest returns, company history, default numbers and my own investing experience. Risk rating explained here.

How Do I Sign Up?

Click here to sign up for Zopa and receive a £50 bonus when you invest £2000. (Zopa pays me a small referral fee at no expense to you. When you sign up for an account through my website, it allows me to continue updating this Zopa review at no cost to you).

The Zopa Review: What You Need To Know

Zopa Review Thumbs Up

- Established 2005 / survived 2008 financial crisis / Over £5 billion lent

- Transparent loan book information

- Existing Access and Classic account loans continue to be Safeguard protected until 2022

- ISA available

- Completely hands-off automatic diversification and reinvestment

- Low default rates

- Possible to exit loans for a fee (never guaranteed)

- Easy to use website with simple investing options

Zopa Review Thumbs Down

- Core account offers no Safeguard Provision Fund

- Plus product interest returns are falling

- 1% exit fee + market rate change fees make exiting expensive

- Loans are unsecured

- Main company operating at a loss and has been for many years

Read more below in my exclusive Zopa review.

Coronavirus Update

Due to changes to market conditions resulting from the Coronavirus pandemic, expect to see low liquidity resulting in slower exit times*. Zopa has also tightened its new borrowers’ lending requirements. Expect to see Zopa receiving large numbers of loan applications but also borrowers asking for temporary loan forgiveness due to financial strains.

* Exiting peer to peer lending investments is never guaranteed as liquidity changes during the varying market and economic conditions.

Equivalent Competitors

Ratesetter, Lending Works, Growth Street

Zopa’s Company Financials

For 2019, Zopa Group Limited reported after-tax losses of £18.1m in losses due to heavy investment in its new start-up bank. Zopa Group Limited’s company accounts can be seen here

Zopa Review: My experiences so far….

I spent several months researching Zopa and their operation before decided to invest with them. Despite opening my account in 2015, I had previously steered clear of Zopa because I was put off by their financial losses as a business. After further research, I decided to give Zopa a try.

I particularly liked Zopa’s growth and the pat actions it took to protect loan quality and lenders’ interest by limiting new investors due to unbalanced demand and supply. Zopa used to limit new lenders by placing them on a waitlist which was frustrating for those wanting to lend money. I haven’t seen these limits in place for quite some time.

This investor limiting shows Zopa’s willingness to maintain their loan quality and protect both their business model and their lenders so I think it is a good move.

Zopa is very simple to use as lenders choose from two products with different risks.

I was surprised to see Zopa discontinue its legacy instant Access and Classic accounts and replace them with the non-Safeguarded Core account. Zopa has always been heralded for being one of the safer peer to peer lending options.

The removal of the Safeguard Funds was a bold decision, that for me, made Zopa too risky an investment proposition for the lower returns offered. Zopa’s also reduced its Plus account returns so I ultimately decided to let my loans mature without further investment.

As part of my exit strategy, I tested Zopa’s exit option in December 2018 and my loans were sold in only 48 hours.

I decided to leave the rest of my funds invested until they mature but I won’t be adding more money at the current return rates. The risk I’m taking in the Plus account isn’t on par with my expected 3-4.3% future returns.

Due to abnormal market and economic conditions caused by the Coronavirus, I expect Zopa to be affected but higher borrower defaults and lower investor demand.

What Is Zopa?

Zopa is a UK based peer to peer lending company that has lent over £5bn since 2005. Zopa facilitates investors lending money to unsecured consumer loan borrowers via two products, Core and Plus. Borrowers can take loans for up to five years. Lenders funds are either split into £10 parts and spread across at least 100 loans (Core product), or lent to a “sensible” amount of borrowers in the Plus product. The three different products offer different return rates due to the varying levels of risk, exit availability and fees.

Hands-off reinvestment of interest and capital repayments happens by a click of a mouse button, so there’s no need to spend time watching your account.

Zopa Limited, Zopa’s peer to peer lending arm, is part of a larger company (Zopa Group) that includes a startup bank.

How Can I Contact Zopa?

Web

Email: contactus@zopa.com

UK Tel: 020 7291 8331

When Did Zopa Launch?

2005

Are They Regulated?

Zopa is regulated by the UK Government’s Financial Conduct Authority #563134 under full permissions granted May 10th, 2017. Remember that peer to peer lending isn’t covered by the FSCS (Financial Services Compensation Scheme). The FCA does have the ability to pursue criminal action against companies that violate its standards, but the FCA is not a government entity and it is funded by the very companies it regulates.

Who Can Open An Account?

Any person 18 years or older who is a UK resident, has a UK bank account and can pass the verification checks.

What’s The Signup Process Like?

Easy; I was verified by providing identification documents and my account was opened within a few hours.

How Much Time Will It Take To Become Invested?

Zopa’s lender loan matching times varies based on demand and loan supply but loan matching times are generally fast.

What’s The Minimum Deposit / Investment?

Zopa Core: £1,000

Zopa Plus: £1,000

All amounts are automatically diversified across many borrower loans so no manual lending is needed. This saves you lots of time.

How Are Deposits Made?

You can deposit via bank transfer which is how deposited. If you are feeling a little old school, you can send a cheque.

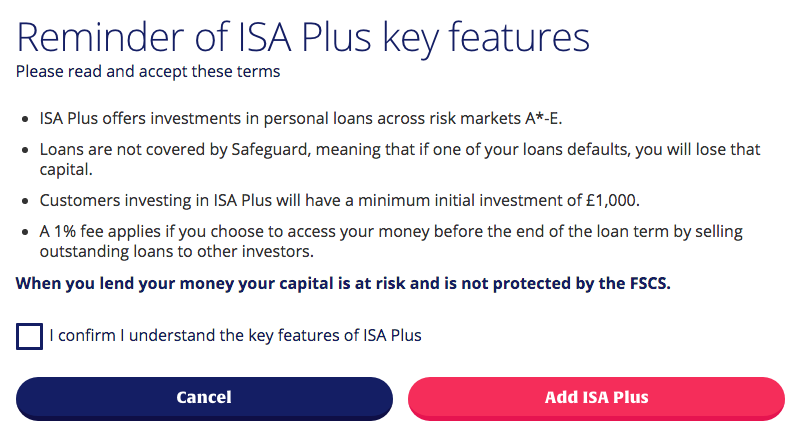

Does Zopa Offer An Innovative Finance ISA?

Yes, and opening an ISA is very simple. From your dashboard, just click the Open An ISA button:

Add a product…

Accept the conditions…

And you’re done.

The ISA’s products are identical to Zopa’s regular account products.

What Are The Different Lender Products?

Zopa Core: Core replaced the Access and Classic accounts. Core has a £1,000 minimum investment and lenders’ funds are split into £10 slices and automatically invested across multiple borrower loans.

No more than 1% of your total deposit will be invested into a single loan. For example, if you deposit £2,000, you will be invested in 200 loans. This provides lenders with instant diversity and lower risk. Borrower risk levels are considered between A and C. The Core account isn’t covered by any Provision Fund so the risk level has increased. If you want to exit your investment, there is a 1% fee*.

Zopa Plus: Plus also has a minimum £1,000 investment requirement and a 1% exit fee*. Plus offers higher returns for those willing to take more risk. Where does the extra risk come from? Borrower risk levels are considered between A and F and the product is not covered by a provision fund.

- Existing customers who were invested in loans through the older Access and Classic accounts prior to discontinuation will continue to be protected by the Safeguard Provision Fund until approximately 2022 when loans mature. All new loans will be through the non-Safeguard protected Core and Plus lending products.

* Exit depends on there being lender demand to buy you out of your loans. Ability to exit is never guaranteed.

How Are My Loans Allocated?

All loans are allocated automatically. Zopa has a pretty detailed information page where you can see exactly which risk bands your money is invested in and the loan time lengths:

Here is a breakdown of my personal portfolio showing returns and how much is invested into each risk band:

| Risk Band | Return Rate | Total % of Portfolio |

|---|---|---|

| A* | 3.3% | 12.3% |

| A1 | 4.5% | 9.7% |

| A2 | 4.7% | 15.2% |

| B | 9.1% | 23.2% |

| C1 | 12.5% | 11% |

| D | 18.3% | 20% |

| E | 25.1% | 25% |

You can even download your entire loan book. From your dashboard click loan book then click the big blue button at the bottom of the page:

How Much Interest Does Zopa Expect Lenders To Earn?

Plus: 4% – 6%

Core: 3.4% – 5%

(Rates change weekly. Return estimations are capital weighted averages minus expected principal losses and any fees.)

My earnings have average 4.6% and my future earning are 3-4.3%, much lower than the estimated returns.

Is Interest Paid Immediately Or When Loans Begin?

Interest accrues as soon as your funds are allocated to loans. If your money is in the loan queue, you will not receive any interest until it is deployed.

When Is Interest Paid?

Interest is paid whenever borrowers make repayments. Borrowers repay both capital and interest on any given day.

Am I Lending To Zopa Or The Borrower?

Zopa is a true peer to peer lending company so lenders have loan agreements with borrowers. Thumbs up to Zopa.

What Are The Fees?

Zopa makes borrowers pay a fee so lenders don’t have to but if you decide you want to exit your investment early, the following fees apply:

Core: 1% loan sale fee + a possible market adjustment fee

Plus: 1% loan sale fee + a possible market adjustment fee

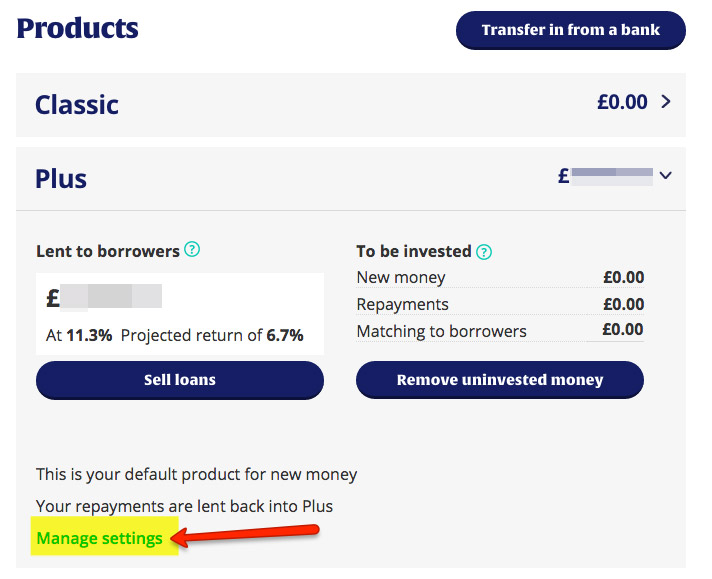

One way to avoid these fees is to simply turn off your reinvestment instructions so when borrowers repay loans early, which they often do, you will be able to withdraw the money from your account for free.

This is how you disable reinvestment from your main Summary page:

- Click the small arrow next to the account you want to change:

2. Click the Manage Settings link:

3. Choose the option:

If you decide to sell your loans you will pay a 1% fee plus a Value Adjustment fee. You’ll be charged this fee if your loans have a lower expected return rate than a new equivalent loan. For example, if you own a £10 loan that you want to sell and the borrower hasn’t been making consistent payments, Zopa can estimate the value of the loan to be £9.50, meaning you would receive £9.50 rather than the £10 you paid for the loan. You may also receive less than your loan’s value if interest rates have changed. This is called a Market rate adjustment fee which you can read more about here.

If you decide to sell your loans you will pay a 1% fee plus a Value Adjustment fee. You’ll be charged this fee if your loans have a lower expected return rate than a new equivalent loan. For example, if you own a £10 loan that you want to sell and the borrower hasn’t been making consistent payments, Zopa can estimate the value of the loan to be £9.50, meaning you would receive £9.50 rather than the £10 you paid for the loan. You may also receive less than your loan’s value if interest rates have changed. This is called a Market rate adjustment fee which you can read more about here.

Here is an example of how much you might pay in sales fees:

Also, note only current loans will be sold.

How Much Time Will I Need To Spend Managing My Investments?

Zero. Zopa is a hands-off product so you won’t need to log into your account very often.

How Long Are The Investment Terms?

Borrowers take loans up to five years but often loans are repaid early. As long as there is lender demand and you are willing to pay the applicable exit fees, you can exit anytime.

Is There A Secondary Market To Buy, Sell And Exit Loans?

Yes, sort of. When you want to buy, the system automatically invests your requested amount into loans. There’s no differentiation between the primary market and resale loans for buyers. To sell, there is a 1% administration fee and being able to sell is based on demand. Selling fees can be high, my recent test showed an estimated sales fee of 6% (see above in the fee section).

During the turbulent times resulting from the Coronavirus, expect variations in selling ability. You can only sell loans if buyers demand exists. I expect buyer demand to be very low until the virus concerns calm.

Remember, even under normal market conditions, exiting is never guaranteed but usually possible.

What Security Does Zopa Lend Against?

Zopa gives personal consumer loans for items such as debt consolidation and weddings. All loans are unsecured.

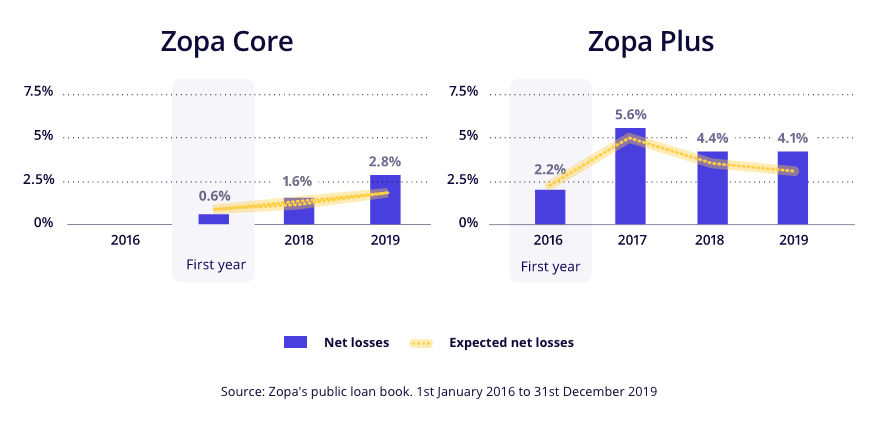

What Are Zopa’s Loan Loss Rates?

Zopa’s worst default year was during the 2008 financial crisis but still, it was only 4.20%. Zopa’s default rates have risen slightly rising but are still within expectations.

Zopa’s worst default year was during the 2008 financial crisis but still, it was only 4.20%. Zopa’s default rates have risen slightly rising but are still within expectations.

You can see current default statistics here.

What Are The Main Risks?

Company Failure: This is a risk with every single peer to peer lending company. If Zopa fails, even though Zopa has made failure provisions, investors could lose all of their money though it’s more likely they would lose some rather than all. Zopa is finally turning a profit and is extremely well funded so failure isn’t likely.

Borrower Defaults: Since Zopa lends to consumer borrowers, defaults are always a possibility. Thankfully Zopa has kept defaults low by lending to credit worthy borrowers.

Lowering of underwriting quality: Zopa’s history has demonstrated a high underwriting quality so I have no reason to think this will change. Zopa used to reject most loan applications but they have eased up on their requirements due to increased competition in the peer to peer space.

Is There A Provision / Safeguard Fund?

Loans within the Access and Classic accounts will continue to be covered by the pre-existing Safeguard Provision Fund until all existing loans have reached maturity. All existing customers were able to buy loans through the Access and Classic accounts until December 2017. After December 217, no new loans were Safeguard protected.

Zopa’s reasoning for eliminating its Safeguard Provision fund has never been clearly explained, although I suspect their fund might have been heavily used as defaults appear to have risen.

It would have been nice for Zopa to reward lenders’ with a return increase since more money should be available with the removal of the Safeguard Fund.

What Happens If Zopa Goes Bust?

Should the worst happen, any un-lent money is held in a bank account separated from Zopa’s assets. Since lenders and borrowers are contracted between each other, borrowers would continue (in theory) to make payments to lenders via the trustee. The trustee would handle the wind-down process and Zopa states that the borrower fee would cover the administration costs of future loan collection.

Usually, I’m somewhat pessimistic when discussing company failure but it seems as if Zopa has provisions in place to protect lenders. Lenders’ may lose some money if the Zopa were to fail so let’s hope Zopa stays in business as a failure would be catastrophic for the peer to peer lending industry.

THUMBS UP FOR ZOPA:

Established 2005 – Safer Peer To Peer Lending Option

Zopa is the oldest known peer to peer lending company and is considered one of the safest since it survived the 2008 financial crisis. Their underwriting team is experienced and seems to be keeping the loan default rates low. From a company longevity perspective, Zopa is relatively safe however because of the upcoming removal of the Safeguard Provision fund, I consider the investments a little riskier now.

Existing Access And Classic Account Loans Will Continue To Be Protected By Safeguard Provision Fund Until 2022

While the discontinuation of the Safeguard Fund is bad news for lenders, at least the fund will continue to cover existing loans until their maturity in 2022.

Information And Loan Transparency

Some peer to peer lending companies aren’t very transparent when it comes to statistics, loan books and data. Zopa, however, is quite the opposite providing full statistics and data. You can view Zopa’s entire loan book here.

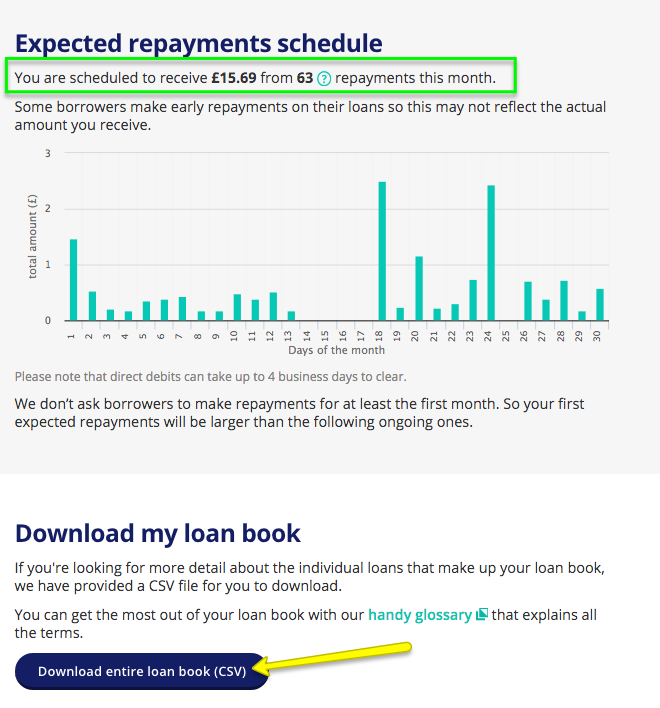

From your account dashboard, you can view your loan portfolio:

And view your expected payment schedule and download your personal loan book to a .CSV file:

This page shows you how many borrowers have missed payments:

From the Loan Book page, you can even download your entire loan book.

I appreciate Zopa’s approach to providing lenders with transparent loan book information.

Completely Hands Off Investing And Reinvesting

Peer to peer lending can be very time-consuming. Zopa eliminates the need for account monitoring by using a set and forget system. Simply choose which product you want to invest in and where you want your repayments and interest to go. You can even decide to reinvest in a different product.

Low Default Rates

Zopa’s high underwriting quality has kept the default rates relatively low. Even during the 2008-2009 financial turmoil, Zopa’s default rates were only a little over 4%. When you consider borrowers are given unsecured loans, the low default rates are impressive.

Secondary Market

Zopa offers lenders a possible exit through their secondary market provided there are lenders to buy your loans. If the interest rates on your loans are lower than current rates, buyers will be credited with the extra amount of interest to offset the difference. The youngest loans are sold first until the requested sale amount has been reached.

Exiting of loans is always based upon the loans being in good standing and there being lender demand, but providing demand exists, simply decide how much you want to sell and let Zopa do the rest. Lender demand has always been strong and I haven’t heard of anyone having a problem exiting their loans.

Don’t forget Zopa charges a 1% exit fee which you can avoid by disabling reinvestment and letting your loans mature (see above).

The Website

It’s very easy to use and looks great. Here is the Portfolio dashboard:

THUMBS DOWN FOR ZOPA:

Low Rates For Increased Risk / Removal Of Safeguard Provision Fund

While savings rates remain at historically dismal levels, Zopa’s Core and Plus products still underwhelm compared to the higher rate offerings by other peer to peer companies. Having said that, the recent rate trends have been rising.

Since the removal of the Safeguard Provision Fund, until rates are in the high 5% range, I consider the Core product to be a poor choice as it’s even riskier. The Plus product used to be more attractive but the lowered rates make it a less attractive choice for the risk involved.

1% Exit Fee + Possible Market Adjustment Fee

If you decide you want to exit your loans, be prepared to pay Zopa’s 1% exit “admin” fee plus a possible Market Adjustment Fee. The Market Adjustment Fee is to offset any interest rate differences from your old loan interest rate to the current rate. (See the explanation in the fee section earlier in the review). Whilst I understand why Zopa has exit fees, I still dislike them.

New Lenders Often Put On Waitlists

Sometimes when lender demand becomes too high, Zopa freezes new investors and uses a waitlist. This will be a source of frustration for those of you who want to give Zopa a try.

Higher Demand Can Mean It Can Take Time To Become Invested

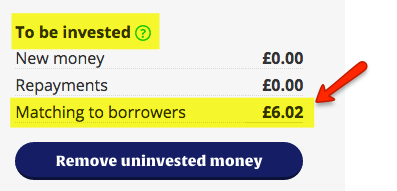

This is true for both new investments and re-investments. If lender demand becomes high, your money could be placed into a queue:

…you won’t earn any interest. Under normal lending conditions, the amount of money in my queue is relatively small.

My initial investment took 15 days to be fully deployed but times can vary depending on demand. This investment deployment time can affect your annual return rates and while it’s hard to say by how much, I predict about -0.25%.

In 2018, queuing hasn’t been an issue but Zopa is very proactive when dealing with excessive lender demand and halts new investor sign-ups when lender demand becomes too high.

Loans Are Unsecured

Zopa’s consumer loans are unsecured which makes the loans more vulnerable during an economic downturn. I have confidence in Zopa’s underwriting standards so I’m not too concerned. Also, Zopa survived the 2008 worst financial crisis and is the only peer to peer lending company to have done so.

Company Operated At A Loss For Years

I believe it’s important to look at a peer to peer companies financial health before investing. It is also important to look at the circumstances behind the company accounts and any future plans.

Since 2005, Zopa has posted losses of over £20 million but most f its losses were due to startup, scale and growth. Thankfully Zopa is well funded by experienced venture capital companies.

In October 2016, Zopa’s CEO announced the company was finally operating at a profit and that it would continue to do so in the future. While this is good news for lenders, it will be nice to see some history of Zopa’s profitability over the next years.

My Strategy

Zopa received my first investment in late 2016. I only invest in the higher paying Plus product because the added risk has netted me 3%+ in expected extra returns. I used to set all capital and interest payments to reinvest but since the return rate targets were lowered to the mid 4% range, I decided not to reinvest.

The low-risk Classic and Access accounts were discontinued in December 2017 in place of the new Core product. I think the removal of the Safeguard Provision fund means increased risks to lenders so I won’t invest in the low interest paying Core account. If you are risk-averse, there may be better options such as Lending Works, Growth Street and even Assetz Capital.

One good thing about Zopa is you don’t need much of an investment strategy. Just choose your product, decide what to do with payments and you are done.

Zopa Review Conclusion

Zopa’s account changes led me to begin exiting the platform because the risks are no longer worth the returns. With the removal of the Safeguard fund, I don’t think the new Core account is worth the risk since the returns are low. I do like Zopa’s strong track record and longevity and I hope that they will continue to lead the peer to peer industry forward.

Despite the downsides, Zopa will still appeal to those looking to place money with a company that has the longest peer to peer lending track record. The ISA will be appealing to those looking for a tax free option. With the account changes, only time will tell if it remains the strong peer to peer lending powerhouse it once was.

I hope you found this Zopa review informative.

Click here to sign up for Zopa and receive a £50 bonus when you invest £2000. (Sometimes Zopa’s lender demand become too high and the company closes to new investors. If this happens, check back frequently. Zopa pays me a small referral fee at no expense to you. When you sign up for an account through my website, it allows me to continue updating this Zopa review at no cost to you.)

If you enjoyed this Zopa review and want to know more about peer to peer lending, click here and receive my complimentary Top 5 Peer to Peer Lending Sites Report.

I love feedback, so if you find any errors or omissions in this Zopa review or you have any improvement suggestions, I invite you to contact me and be a part of contributing to this website.

Disclaimers: I’m not paid to write this Zopa review, nor am I employed by any of the companies I write about. In most cases, I have invested or continue to invest my own money through the companies I write about. The sign-up links on this Zopa review and this website are referral links. When you sign up for an account through my website, I receive a referral fee directly from the companies, at no cost to you. Your support enables me to continue to operate the Financial Thing website. You can read more about my referral links here.

** This Zopa review is for information purposes only and should not be regarded as investment advice. Opinions expressed in this Zopa review are opinions based from my own personal experiences investing my own money. As with any financial investment, peer to peer lending involves risks, so never invest more than you can afford to lose. **