Octopus Choice Review

** Octopus Choice review updated July 16th, 2020 **

— Covid-19 Update: Octopus Choice is closed to new investors and has temporarily suspended all platform transactions. —

Octopus Choice had been off my radar until a visit to their London offices where I was impressed. Octopus Choice is an arm of the far larger Octopus Group company which has businesses in property lending, venture capital, financial investing, healthcare, energy and technology development. I was surprised by the size of the Octopus Group operation which employs over 800 people.

I had been dabbling in Octopus Choice with a very small investment amount for a few months, but after my visit, I’m far more intrigued by the company. Read on for my full Octopus Choice review.

My Current Investment Amount: Click here

My estimated annual rate of return: 5.6% (Covid Increased Rates after fees but before taxes)

[table “38” not found /]* This opinion risk factors in loan types, interest returns, company history, default numbers and my own investing experience. Risk rating explained here.

How Do I Sign Up / Any Bonuses?

— Covid-19 Update: Octopus Choice is closed to new investors and has temporarily suspended all platform transactions. —

Click here to sign up for Octopus Choice. (No current cashback offers. When you open an account through my website, it helps me to continue to offer new reviews and update existing ones).

The Octopus Choice Review: What You Need To Know

Thumbs Up

- Loans secured by property

- Reasonable loan to value percentages (60%)

- Octopus Choice invests 5% of their own capital into each loan

- Transparent loan book shows borrower interest rates

- Financially stable company profitable and debt free / part of the much larger Octopus Group

- Lender dashboard shows status and info of every loan you’re invested in

- Website is incredibly easy to use

- Zero fee early exit possible (not available during Covid-19 market conditions)

- Auto diversification across multiple loans that increases over time

Thumbs Down

- Lower lender % returns within the peer to peer industry (Pre Covid)

- Some of my money is tied up in defaulted and late loans

- Loan book doesn’t detail property type or address

Read more below in my exclusive Octopus Choice review.

Coronavirus Update

Due to the Coronavirus crisis, Octopus Choice has temporarily frozen all transactions, new investments and is not currently accepting new investors. The platform fee has also been temporarily suspended therefore increasing targeted investor return rates from 4.1% to 5.5%. Current investors can withdraw interest payments and uninvested money sitting in their holding accounts.

Alternative Companies

Octopus Choice’s Company Financials

Octopus Choice made a post-tax profit of £2,178,220 for the year ending April 30th, 2019. The company has zero debt which makes Octopus Choice an enticing company to invest through. Company accounts can be seen here.

Octopus Choice Review: My experiences so far…

I made my first small investment through Octopus Choice in November 2016. I was reluctant to invest too much money into Octopus because they weren’t on my radar and I thought the return rates were too low, but after my visit to the Octopus Choice offices in September 2018, I decided to dip my toe in the Octopus filled waters. Their operation backed by Octopus Investments, company culture, property-backed investments and technology capabilities were impressive.

I invested a small amount of money to begin. My only gripe is a portion (approximately 5%) of my investment seems to be frozen because the funds are invested in loans which are late or in collections.

During Covid-19, all transactions have been suspended through Octopus Choice which means no exiting from existing investments. This freeze move hasn’t surprised me as it was put in place to protect investors and the Octopus Choice. I’m comfortable leaving money invested.

What Is Octopus Choice?

Octopus Choice is a lower risk peer to peer lending company that offers a simple peer to peer lending product backed by a portfolio of property secured loans. There is only one product choice which is an auto-invest product. Deposit money and Octopus Choice picks out your loans and auto-diversifies.

How Can I Contact Octopus Choice?

Octopus Choice website

Email: support@octopuschoice.com

UK Tel: 0800 294 6848

When Did Octopus Choice Launch?

April 2016

Are They Regulated?

Yes, by the Financial Conduct Authority #722801 under full permissions granted December 22nd, 2016. Investments made through Octopus Choice are not covered under the FSCS (Financial Services Compensation Scheme). FCA regulation is nothing like the FSCS, which covers consumers when they deposit money in banks. The FCA reports to the UK government and has the ability to pursue criminal action against companies which violate its standards and codes of conduct.

Who Can Open An Account?

Any person 18 years or older who has a UK bank account and can pass the verification checks.

What’s The Signup Process Like?

Octopus Choice runs the usual anti-money laundering checks. Just go through the motions and provide UK resident and banking information.

What’s The Minimum Deposit / Investment?

Minimum deposit: £10

Minimum investment: £10

How Are Deposits Made?

Deposits are made instantaneously via a debit or credit card or you can make a non-instantaneous bank transfer.

Does Octopus Choice Offer An Innovative Finance ISA (IFISA)?

Yes

What Types Of Lending Products And Accounts Does Octopus Choice Offer?

Octopus Choice only offers one lending product. It’s an auto investment product whereby you deposit money and Octopus spreads your money across multiple loans. Currently, my investment is spread over 54 loans.

How Much Gross Annual Interest Are Lenders’ Paid?

This varies but tends to be in the low 4% range.

How Long Will It Take My Money To Be Invested?

Octopus Choice invests money over a minimum of ten loans so money deployment depends on demand and supply. I deposited money on October 13th, 2018 and that money was 100% deployed within one business day.

Is Interest Paid Immediately Or When the Loan Starts?

Interest is paid when your money is deployed.

When Is Interest Paid?

Interest is paid monthly depending on when your money is deployed. Mine is paid on the 10th or the 11th of each month.

Am I Lending To Octopus Choice Or The Borrower?

Octopus Choice is a true peer to peer lending company so you are loaning money directly to borrowers rather than to Octopus Choice the company.

What Are The Fees?

All fees are paid by loan borrowers

How Much Time Will I Need To Spend Managing My Investments?

Zero as Octopus Choice’s lending product is 100% automatic

What Security Does Octopus Choice Lend Against?

Octopus Choice’s loans are all secured by property sourced by its in-house Octopus Property arm. The maximum loan-to-value is 76%, but the majority of loans have ltv’s between 50% and 70%. If the borrower defaults, Octopus Choice can use its legal charge to take over the property and attempt to recover capital and interest.

Tell Me More About Octopus Choice’s Loan Book

Octopus Choice publishes its loan book and is mostly transparent about its contents including property valuation, loan amount, loan to value, loan start and end dates, and borrower and lender interest rates. Loan amounts go as high as £8m but the average loan size is about £600,000 with an average loan-to-value of 64% with an average term of 3.8 years. You can see current statistics here.

Due to the low average 64% LTV, theoretically, property prices would need to fall by 40% on the average loan for an investor to lose any capital

What Are The Loan Default / Loss Rates?

Octopus Choice has a very low default rate with only 0.72% of their loans paying late. As of March 2019 here are my loan statistics: loans have defaulted.

53 loans are performing as expected

3 loans are late

1 loan is in collections

You can see current statistics on their website.

What Are The Main Risks?

Company Failure: This is a risk with every peer to peer lending company, especially ones with smaller loan books. If their business model fails, investors could lose all of their investment though it’s more likely they would lose some of their investment.

Economic downturn: Octopus Choice has yet to experience a severe downturn in the economy. If a downturn were to occur, Octopus Choice might experience higher borrower default rates.

Valuation issues: Some peer to peer companies have struggled to obtain accurate RICS property valuations. If the valuations are incorrect and the property defaults, there may be a shortfall in default recovery amounts.

Borrower defaults: If borrowers stop making loan payments, a default process is put into motion. Property default recovery can be lengthy, sometimes running into years.

Is There A Provision Fund?

Octopus Choice doesn’t have a provision fund but it invests 5% of its own money into each loan so you can consider this a first loss fund. This means if a loss is experienced on a loan, the first 5% loss will be taken by Octopus Choice.

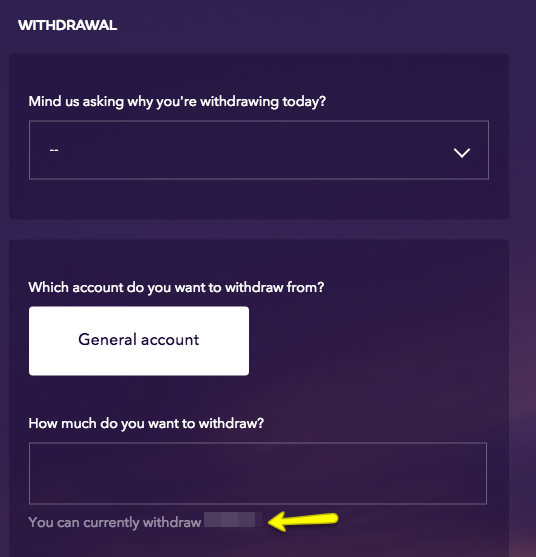

Is There a Secondary Market For Exiting?

Octopus Choice doesn’t have a dedicated user market for exiting loans. What Octopus Choice will do is place your loans for sale and if availability exists, you will be able to exit. Octopus Choice will even buy your loans themselves if they are able to. When you click on withdrawal from your lending dashboard, you can see how much of your balance is available for withdrawal:

What Happens If Octopus Choice Goes Out Of Business?

Octopus Choice states on its website that all security charges over properties are held in trust. In the event of insolvency, a third party would be put in place to handle the wind-down of the company and the loans. When a peer to peer company goes out of business, there are many unknown variables that can affect how much capital lenders’ might be paid back. See the Collateral situation for an example of this.

THUMBS UP FOR OCTOPUS CHOICE

Loans Secured By Property / Low Default Rates

Octopus Choice’s loan book is made up of property sourced by its in-house team. Each of these properties is secured by a legal first charge which Octopus Choice can enforce if the borrower defaults on its payments. Once the property is controlled by Octopus Choice, it can be sold to recover capital and interest.

Octopus Choice has a history of low default rates due to the properties and borrowers it chooses to lend to.

Lower Risk / Transparent Loan Book Shows Borrower Interest Rates

Octopus Choice seems to underwrite loans that have reasonable loan-to-values. You can see this by downloading their entire loan book which lists all pertinent loan information. The spreads between what the lender makes and what the borrower pays are also reasonable indicating these borrowers are lower risk. There are no 20% interest rates within the loan book and most spreads are about 4%.

Octopus Choice Invests 5% Of Its Own Capital In Each Loan

Octopus Choice puts its money where its mouth is and invests in each loan it underwrites. The 5% investment is a good indication of the confidence the company has in its loans. The investment is also extra revenue for the company and we all know a profitable company is better than an unprofitable one. Finally, the 5% investment is a first loss, meaning that if a property loan deal experiences a financial loss due to a default, Octopus Choice will take the first 5% loss.

Financially Stable, Well Funded Company / Part Of The Much Larger Octopus Group

Due to the collapse of Lendy and Funding Secure, I’m paying close attention to the financial stability of peer to peer to companies. Octopus Choice appears to be one of the most stable companies in the peer to peer sector.

When I visited the offices of Octopus Choice in September 2018, I was impressed by the size of their operations. Octopus Choice is an arm of the much larger Octopus Group which employs over 800 people. Octopus Group is made of a group of companies which services the finance, healthcare, energy and technology sectors.

Octopus Choice is well funded by the Octopus Group which has over £6 billion under asset management. When a company is well funded it can grow and expand through times of unprofitability. Octopus Choice is also profitable and reported zero debt in its company accounts.

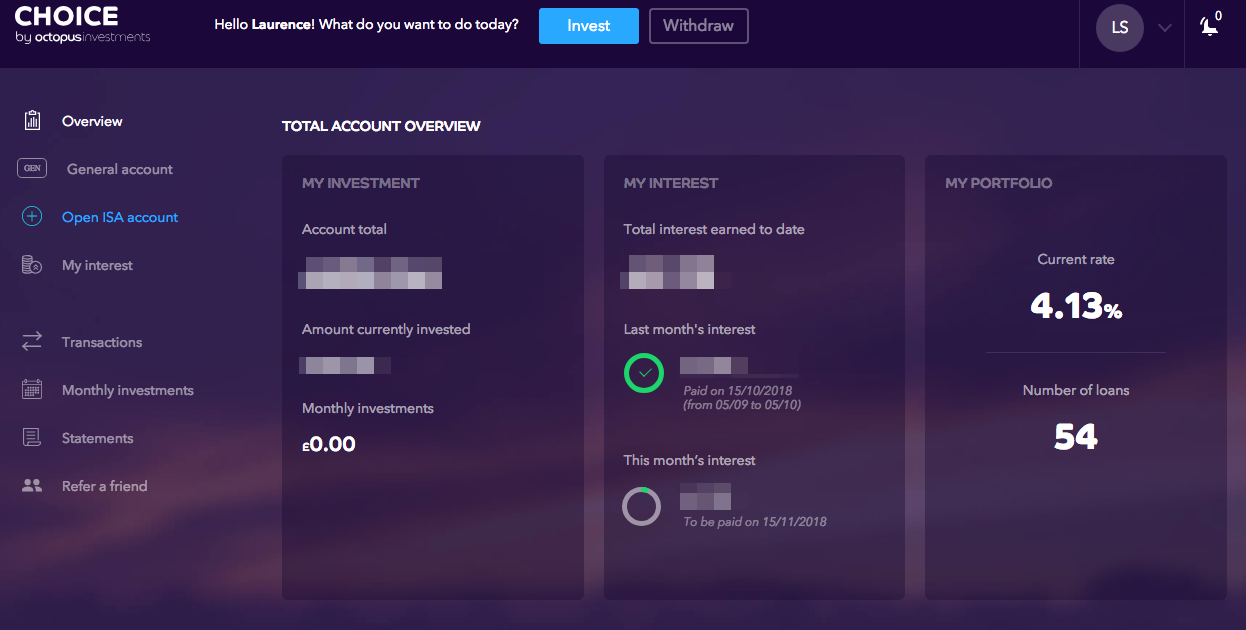

Lender Dashboard Is Well Laid Out And Shows Every Loan You Are Invested In Including Status

Octopus Choice’s dashboard is very easy to use and provides most of the information to track the performance of your investment including the expected return rate, the number of loans you are invested in:

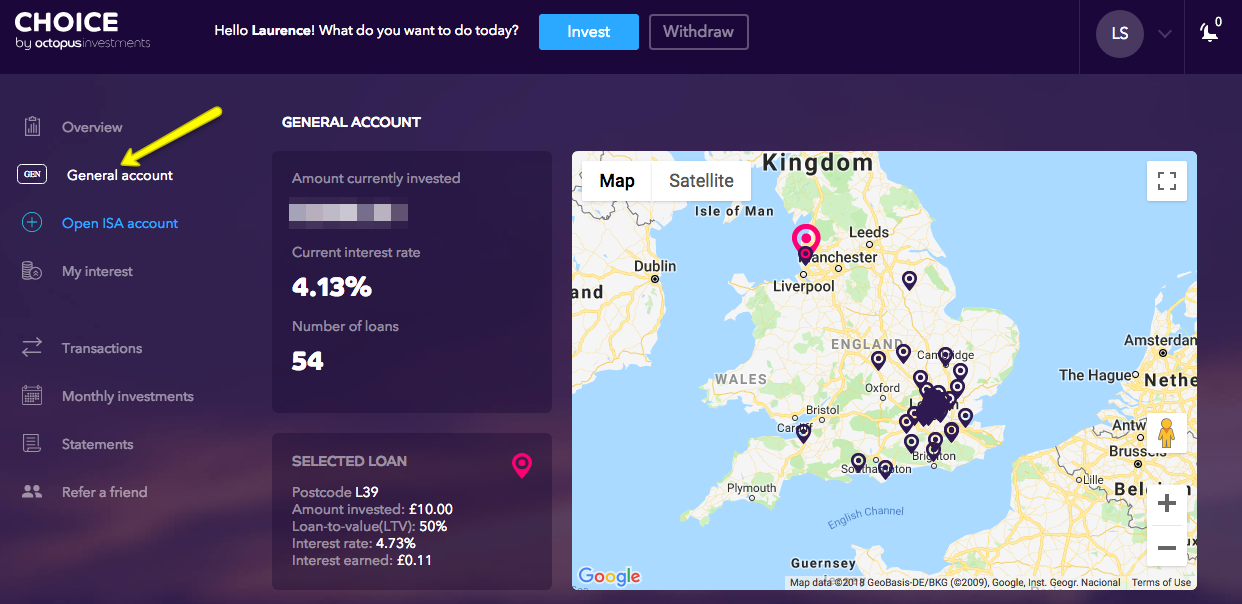

Want to see your loan portfolio and loans statuses? Just click on the General Account option:

Zero Fee Exit Early Exit Possible

Not all peer to peer lending companies offer an exit but Octopus Choice does, despite it not being guaranteed. If you want to sell, you can do so by simply pressing the withdrawal button. Your lender dashboard displays how much of your investment is available for withdrawal. Octopus Choice then places this amount for sale and if there is demand, your requested amount is sold for no fee. Octopus also states on its website that it will buy requested loan parts if possible. Again no guarantees here.

Loans Secured By Property

All of Octopus Choice’s loans are secured by property so if the borrower defaults, the capital and interest can try to be recovered by selling the property.

THUMBS DOWN FOR OCTOPUS CHOICE:

Lower Returns In Peer To Peer

With safety comes downsides in the form of lower returns. Octopus Choice’s returns were in the low 4% range (Pre-Covid) and have been temporarily bumped to around 5.5% during Covid. The reason for this rate increase is due to the suspension of the platform fee which is paid by borrowers.

A Portion Of Your Investment Will Likely Be Frozen For Withdrawal

If a loan falls late or into default, you won’t be able to withdraw that portion of money from your account. Once the loan is brought up to date or recovered, that portion of frozen money should be made available again.

Loan Book Doesn’t Show Property Details

While Octopus Choice publishes its entire loan book, there’s no information about the types of properties loaned against or the addresses. Only the first three letters and numbers of the postcode are given. It would be nice if property addresses and types were listed.

My Strategy

The beautiful thing about Octopus Choice is there’s no strategy needed. Just deposit money and collect your monthly interest. I do keep an eye on the availability of my funds for withdrawal to see how the loans are performing but I currently, have no fears about my investment through Octopus Choice.

I am pleased Octopus has suspended its platform fee and raised investor targeted returns during the Covid-19 pandemic.

Octopus Choice Review Conclusion

Octopus Choice is very financially stable being financially backed by the much larger Octopus Group which is made up of health care, energy, and financial technology companies. Octopus Choice is profitable with zero debt and is positioned to be a lower risk, lower reward peer to peer lending product.

Octopus Choice is a hands-off peer to peer investment, easy to use and secured by property with reasonable low-to-values.

It would be nice for all funds to be available for withdrawing but it’s rare for a peer to peer company to have zero late loans or defaults.

Octopus Choice’s returns are in the lower end range of peer to peer investing but the risk is much lower so I’m willing to make it part of my diversified peer to peer lending portfolio as long as the defaults stay at a low level.

Despite suspending platform transactions due to Covid-19, I have high hopes Octopus will resume normal market activities and I will continue to invest through them.

— Covid-19 Update: Octopus Choice is closed to new investors and has temporarily suspended all platform transactions. —

Click here to sign up for Octopus Choice. (No current cashback offers. When you open an account through my website, it helps me to continue to offer new reviews and update existing ones).

If you enjoyed this Octopus Choice review and want to know more about peer to peer lending, click here and receive my complimentary Top 5 Peer to Peer Lending Sites Report.

I love feedback, so if you find any errors or omissions in this Octopus Choice review or have any improvement suggestions, I invite you to contact me and be a part of contributing to this website.

Disclaimers: I am not paid to write my reviews and I’m not employed by any of the companies I write about. In most cases, I have invested or continue to invest my own money through these companies. In order to keep the website financially viable, the sign-up links on this website are referral links and I do accept advertising in the form of banner ads.

This advertising in no way influences my reviews and opinions. When you sign up for an account through my website, in some cases I receive a referral fee directly from the companies, at no cost to you. Your support enables me to continue to operate the Financial Thing website. You can read more about my referral links and banner advertising here.

** This Octopus Choice review is for information purposes only. This information is not financial advice and has been prepared without taking your objectives, financial situation or needs into account. You should consider its appropriateness for your circumstances. All investing carries risks. Opinions expressed in this review are opinions based on my own personal experiences. The FSCS does not cover peer to peer lending and your capital is at risk. Please don’t invest more than you can afford to lose. **