Loanpad Review

** Loanpad review updated March 20th, 2025**

Welcome to my unbiased Loanpad review where I highlight all the good and bad things investing through Loanpad. I have been investing my own money in Loanpad’s loans since early 2019.

I first became interested in Loanpad after I met with the CEO and founder Louis Schwartz in the summer of 2018. Loanpad’s unique daily-interest-paying peer to peer lending products offers quick access and 60-day access options (based on market conditions) via a low-risk lending model.

Even during the harsh pand-economic times, Loanpad has maintained low default levels and high levels of liquidity allowing for investors to exit if needed (liquidity can change at any time).

I once again met with Louis in January 2019 and he gave me an in-depth tutorial on Loanpad’s dashboard as well as a fully transparent explanation of Loanpad’s products and loan sources. After my meetings with Louis, I liked Loanpad’s approach to reduced peer to peer lending risk and I decided to invest my own money through Loanpad’s products.

Loanpad is the only peer to peer company I use that pays interest into investors’ accounts daily.

My Current Investment Amount: Click here

My current gross annual rate of return: 6.5%

| Est. Annual Returns: | Up to 6.5% |

| My Risk Rating *: | |

| Launched: | 2019 |

| Early Exit: | ✓ |

| Autoinvest: | ✓ |

| ISA Available: | ✓ |

| Loan Security: | Property |

| Provision Fund: | ✓ (Small) |

| Lender Fees: | Up to 0.5% Premium Account exit fee |

| Min Investment: | £10 |

| Time to Become Invested: | Fast |

| Time Needed Managing: | Minimal |

| FCA Regulation: | Full |

| Account Sign Up: | Sign up |

* This opinion risk factors in loan types, interest returns, company history, default numbers and my own investing experience. Risk rating explained here.

How Do I Sign Up?

Click here to sign up for a free Loanpad account

(When you open an account through my website, it helps me to continue to operate and offer new reviews).

My Loanpad Review: What You Need To Know

Thumbs Up

- Two simple lower-risk products, Classic (easy access) and Premier (60-day access). £10 min. ISA available

- Maintained liquidity and low default rates throughout pandemic

- Loanpad takes a senior tranche position over lender on every loan

- Loan-to-value ratios are low (max 50%)

- Sourced lender invests between 25% – 50% of own capital into each loan

- Interest paid into your account daily / Auto Lend reinvestment

- Your funds are automatically diversified across all loans

- CEO’s legal background has given him extensive experience in property development lending deals

- Loans are sourced from a conservative lender with 40+ years of experience that Loanpad’s CEO has been working with for over 12 years

- 19 lending partners

- Loanpad is well funded and profitable

Thumbs Down

- Some cash drag occurs due to £10 min reinvestment

- All eggs in the property development basket

- Auto Lend interest can only be paid into one account type (not good for those who use Classic and Premier at the same time)

While Loanpad won’t break any yield records due to its lower risk product, I believe Loanpad is one of the best offerings if you want a lower risk peer to peer lending product that pays daily interest.

Read more below in my exclusive Loanpad review.

Loanpad Review: My experiences so far…

I made my first Loanpad investment in January 2019, a few weeks after launch. My money was received quickly and was invested in about 24 hours. I invested through both the Classic and Premier accounts. I’ve been receiving interest payments daily and everything has been running smoothly from day one.

I’ve had great communication with Loanpad’s CEO and believe Loanpad’s business model is lower risk and sustainable.

You can watch my Q&A session with Loanpad’s CEO here.

Loanpad has maintained excellent liquidity. Even through the pandemic crisis and I was able to exit loans and withdraw funds as needed. (Remember exit is never guaranteed).

While Loanpad’s investor rates were reduced in 2020, the rates have risen to competitive levels in 2023.

How Much Gross Annual Interest Are Lenders’ Paid?

Classic Account: 5.5%

Premier 60 Day Access Account: 6.5%

Same for IFISA’s

What Is Loanpad?

Loanpad is a UK based peer to peer lending company that sources property development loans from its trusted lending sources whom CEO Louis Schwartz has been working with for over many years. Loanpad offers two simple auto-invest products that pay interest daily. All investments are property backed with max loan-to-values of 50% and with the loan borrower investing a minimum of 25% of its own funds into each loan.

Loanpad, in my opinion, is in the lowest peer to peer lending risk tier.

How Can I Contact Loanpad?

Email: support@loanpad.com

Live chat available on the website

Tel:0203 829 4541

When Did Loanpad Launch?

January 2019

Are They Regulated?

Yes, by the Financial Conduct Authority #741576 under full permissions granted May 5th, 2018. Investments made through Loanpad are not covered under the FSCS (Financial Services Compensation Scheme).

FCA regulation is nothing like the FSCS, which covers consumers when they deposit money in banks. The FCA reports to the UK government and has the ability to pursue criminal action against companies which violate its standards and codes of conduct.

Who Can Open An Account?

Any person 18 years or older who has a UK bank account and can pass the verification checks. If you live in a foreign country and you have a UK bank account, you can apply.

Can I Open An Account Under A Company?

Yes, Loanpad accepts company accounts. When you applym a company account selection is an option.

What’s The Signup Process Like?

Loanpad runs the usual anti-money laundering checks. I was able to open my account in a few minutes. I found the verification and account opening process to be quick and simple. Overseas investors are welcome but they must have a UK bank account.

What’s The Minimum Deposit / Investment?

Minimum deposit: £10

Minimum Investment: £10 and multiples of £10

How Are Deposits Made?

Via bank transfer only but they are usually deposited within one business day. Transfers only occur on non-holiday business days.

Does Loanpad Offer An Innovative Finance ISA (IFISA)?

Loanpad offers an IFISA wrapper that can be used for both its investment products.

What Types Of Lending Products And Accounts Are Offered?

Loanpad offers two simple lending products:

Classic Account: This is designed to operate like an easy access product that allows you to withdraw your money on request. It’s very important to understand this product isn’t like your high street bank savings account. Withdrawal availability is always based on market conditions and is never guaranteed. The Classic Account pay lowers interest versus the Premier Account.

Premier Account: This is a 60-day access product that pays higher interest than the Classic Account. Again, the ability to exit is based on demand and supply but so far, liquidity hasn’t been an issue. This Premier account is my preferred account.

Both accounts automatically spread your money across all the property development loans on the platform.

When you have money in your cash balance, withdrawal requests are usually processed in one business day but can take up to three business days. You can now use the auto-withdrawal feature which occurs once per month on a date of your choosing.

Is Interest Paid Immediately Or When the Loan Starts?

Interest accrues once it is invested into the Classic or Premier accounts. Interest does not accrue on the money inside your Cash account.

When Is Interest Paid?

Interest is paid daily at 12pm. Daily interest payments are a great perk.

Is There A Secondary Market

Yes. You can request to exit from the Classic account anytime (based on liquidity) and from the Premier account with 60 days notice. Exit availability depends on demand and supply but I haven’t heard of anyone not being able to withdraw money if they’ve needed to. Just remember that exiting is never guaranteed and in order to exit, there has to be someone willing to take your loans which Loanpad facilitates.

Am I Lending To Loanpad Or The Borrower?

Loanpad is a true peer to peer lending company so you’re loaning money directly to borrowers rather than to Loanpad the company.

What Are The Fees?

Loanpad doesn’t directly charge investors fees but it does take a small margin from borrowers interest payments.

If you need to withdraw early from the 60-day Premier account, Loanpad charges up to 0.5% of the amount you’re withdrawing. They are hoping to reduce this fee to 0.2% in future.

How Much Time Will I Need To Spend Managing My Investments?

Loanpad now offers auto lend reinvestment so you won’t need to spend any time managing your investment.

How Long Are The Investment Terms?

Classic Account: No minimum

Premier Account: 60-Day notice

Does Loanpad Offer Auto Re-investments Or Withdraw?

Yes to both. The auto lend feature automatically reinvests your interest and capital payments. The payments are sent to your Cash account until there is £10 balance, at which point the money is reinvested into the account type of your choice. This £10 balance will soon be reduced to £1 making reinvesting faster for those with lower investment balances.

If you use both account types you can only choose one account type for reinvestment:

Loan pad also offers monthly auto withdraw where you can set which date the payment is made into your designated bank account:

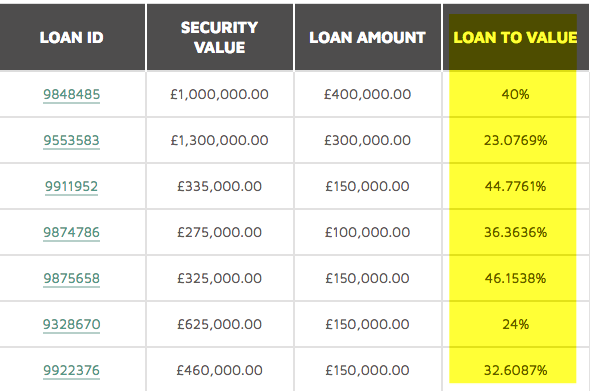

What Security Does Loanpad Lend Against?

Loanpad secures each loan as the senior debt holder on the property it loans money against. Loanpad’s loan-to-values (ltv’s) are much lower than other peer to peer lending companies:

If the valuations are accurate, the lower the loan-to-values, the lower the loan risk.

What Are The Loan Default / Loss Rates?

Zero

What Are The Main Risks?

Company Failure: If Loanpad fails, investors could experience losses.

Economic downturn: Loanpad has continued to operate through a severe economic downtown due to the pandemic. Because Loanpad is well positioned due to its strong first position charge and low loan-to-values, the business has operated well and I don’t expect it to be as affected by a recession as other peer to peer lending companies might be.

Valuation issues: RICS property valuations are opinions and can be inaccurate. If the valuations are incorrect and the property defaults, there may be a shortfall in recovery amounts and investor capital losses.

Is There A Provision Fund?

Loanpad has a small Interest Cover Fund (ICF) to help cover any interest payments that are missed due to borrower late payment or default. It’s important to know that this fund only covers interest payments and not the actual money you have invested inside a loan.

The ICF is really just an added bonus. Because the loan borrower has significant skin in the game, therefore reducing the loan-to-values, provision funds such as the ICF become far less important.

What Happens If Loanpad Goes Out Of Business?

Loanpad is required by the FCA (Financial Conduct Authority) to have a sufficient wind-down plan in place. If Loanpad were to go out of business, there is an agreement with a third-party service provider to manage all loan agreements so interest payments are maintained. In addition to this, an administration company would work on behalf of the creditors (people owed money by Loanpad) and customers (borrowers) to recover as much money as possible. It’s important to know that we (lenders) are not considered creditors.

All monies in investor Cash accounts are ring-fenced inside a Barclays UK account.

Though unlikely, there are many unknowns that can occur when a peer to peer company goes out of business. As with any investment, be aware that your capital is at risk.

You can read more about Loanpad’s wind-down procedures in the FAQ section.

LOANPAD THUMBS UP

Two Simple Investing Products

Loandpad is very easy to use as it offers two simple products with a £10 minimum investment. Just select the Classic or Premier account (or use them both) and off you go. You can easily transfer money between the two products should your needs change.

Interest Paid Daily Into Your Account

Loanpad is the only peer to peer lending company I know of that pays daily interest. This is great for people who are looking for regular income payments.

Exit Liquidity

Throughout the pandemic, Loanpad was one of the few companies that maintained excellent liquidity and exit options for investors. Exit times have remained one day or less. This is a testament to Loanpad’s business. Remember that being able to exit your investments is never guaranteed.

Your Funds Are Automatically Diversified Across All Loans

When you invest money into either the Classic or Premier accounts, your money is automatically spread across all loans on the platform. The amounts are weighted versus the size of the loan.

For example, 3.4% of my money is invested in a £2.4m loan while 0.14% is invested in £100,000 loans.

The longer you remain invested and the more loans Loanpad offers, the more diversified your investment will automatically become.

CEO’s Legal Background In Property Development

Loanpad’s CEO and founder, Louis Schwartz, is a lawyer who has worked on property development deals for most of his career. This means he has a deep understanding of how loans should be structured and administered. This should bode well if any of the loans fall past due.

19 Lending Partners With Decades of Lending Experience

Loanpad’s main lending source (Handf) is a family-owned lending business established in the 1980’s, with hundreds of deals under their belt. Handf keeps loan to value ratio’s at a sensible level, only lends to developments located in places they understand.

Handf also has a previous history in developing their own real estate projects and Louis has worked on the legals for Handf’s lending deals for over 12 years.

Loanpad now has a wide array of borrowing sources which gives further loan diversification.

Loanpad Has A Senior Tranche Position On Loans

This is a very big plus for investors as it reduces risk. Loanpad’s tranche position comes before the lender. This means if a loan were to fall into trouble, Loanpad would legally be in the first position to be repaid after the recovery process.

Loandpad’s Lender Invests Between 25-50% Of Its Own Money Into Each Loan

Another big plus for investors that reduces risk. Since Loanpad’s main lending source, Handf, invests its own money into each loan, the loan-to-value ratio is reduced considerably. Also when the lender has skin in the game, they have more to lose and will be more inclined to chose sensible development projects in order to protect the investment.

Loan To Values Are Lower (LTV’S)

Currently, ltv’s tend to average below between 40-43% across the loan book with a maximum of 50%. These ltv’s are much lower than some other development loans I have invested through other peer to peer lending companies. When the average ltv is low, the risk is lower providing the valuations are sensible which I believe they are.

Loanpad Is Well Funded And Expected To Be Profitable In A Shorter Time Period

Companies need to make a profit in order to survive long-term. Loanpad is well funded by outside investors for continued growth. Since Loanpad doesn’t underwrite their development loans, their expenses are much lower so Louis estimates running at profitable levels in a period of months rather than years.

Loanpad also raised capital through Seedrs.

LOANPAD THUMBS DOWN:

All Eggs In Property Development And Bridging Loan Basket

Loanpad’s loans are all property and bridging loans so there isn’t any diversification in other sectors such as business and consumer lending. You can diversify by investing through other non-property loan based peer to peer companies.

Auto Lend Options

Loanpad launched its auto lend feature in July 2019. There are a few quirks with the feature but I have a feeling these will be fixed as time passes.

One such quirk is there is a £10 minimum reinvestment so until you have £10 in your cash account, your funds won’t be invested. This £10 minimum should be reduced to £1 which is but this hasn’t happened yet.

Secondly, if like me you use both account types, you can’t have payments from those accounts go back into those two accounts. For example, if you want your Classic Account repayments to go back into the Classic Account and your Premier Account repayments to go into your Premier Account, you can’t. Loanpad only allows you to choose one account type for reinvestment. Not a big deal but worth mentioning.

My Strategy

Loanpad is so simple it doesn’t require a strategy. I used to mix my investments between the Classic and Premium accounts but now I mostly use the Premium account with the 60 day access notice. I’ve received my daily interest payments as promised since I began investing in 2019. So far so good.

I’ve was very pleased to see Loanpad continuing to operate as normal through the pandemic and liquidity has remained excellent with exit times at less than one day.

Loanpad Review Conclusion

I remain invested in Loanpad and have been pleased to see interest rates increases and the risk remaining at the lower end. The interest rate rises have made Loanpad more competitive versus other peer to peer learning platforms offering higher rates.

Loanpad offers two lower risk peer to peer lending products that anyone can use as part of a diversified lending portfolio. After meeting with CEO Lous Schwartz several times, I’m comfortable with Loanpad’s business model. I love the fact that Louis has extensive legal knowledge and experience in real estate lending.

I also like that Louis has a long-term relationships with some of the borrowing sources Handf and Blockvale.

I’m very happy the auto lend feature has been introduced and I’ll be even happier when the minimum reinvestment amount is reduced from £10 to £1 to reduce cash drag for those with smaller account balances.

Importantly, Loanpad has remained completely liquid throughout the pandemic, offering investors access to their money within one business day. Remember liquidity can change quickly and exit is never guaranteed.

Loanpad’s low loan to values and conservative approach to peer to peer lending make it a place I’m happy to park my money and Loanpad remains on my Top 5 list.

Click here to sign up for a free Loanpad account

(When you open an account through my website, it helps me to continue to operate and offer new reviews).

If you enjoyed this Loanpad review and want to know more, click here and receive my complimentary Top 5 Peer to Peer Lending Sites Report.

I love feedback, so if you find any errors or omissions in this Loanpad review or have any improvement suggestions, I invite you to contact me and be a part of contributing to this website.

Disclaimers: I am not compensated to write my reviews and I’m not employed by any of the companies I review. In most cases, I have invested or continue to invest my own money through the companies I review. In order to fund Financialthing.com, this website contains referral links and I do accept advertising. This advertising in no way influences my reviews and opinions. When you sign up for an account through my website, in some cases I receive an affiliate referral fee directly from the companies, at no cost to you. Your support enables me to continue to operate the Financial Thing website. You can read more about my referral links and advertising here.

** This Loanpad review is for information purposes only. This information is not financial advice and has been prepared without taking your objectives, financial situation or needs into account. You should consider its appropriateness for your circumstances. All investing carries risks. Opinions expressed in this review are opinions based on my own personal experiences. The FSCS does not cover peer to peer lending and your capital is at risk. Please don’t invest more than you can afford to lose. **