Kuflink Review

** Kuflink review updated Jan 13, 2026**

In August and November 2025, the FCA posted restriction notices on Kuflink Ltd.

1. Kuflink must not without the prior written consent of the FCA, on board any new clients.

2. Kuflink must immediately close its auto invest product to any further money from investors and cease all lending.

I have paused all Kuflink investment and would not recommend any investor transact in any Kuflink loans until we have clear information about what is going on inside the company.

____________________________________________________________

Below is my old review of Kuflink for informational purposes only.

Welcome to my Kuflink review. I had been researching Kuflink for a while and decided to dip my investment toes into the Kuflink water in early 2018 and have been investing in their offered loans ever since.

Kuflink’s founders have been investing in property for 20 years and their private bridging arm has been lending money to property developers since 2011. The peer to peer lending business was launched in May 2016 and has been gaining favour with peer to peer lenders since. Kuflink have lent out over £400m and investors have averaged over 8% interest returns annually. Kuflink has hired a new CEO as previous Head Narinder Khattoare has moved on from the company.

I took a trip to Kuflink’s offices for an office tour and a sit down with former CEO Narinder, Hari (CTO) and Amy (former Legal Executive).

In 2025, Narinder left Kuflink to pursue other ventures.

Watch my latest interview with Kuflink’s CTO Hari and Head of Collections Nattalie

My Current Investment Amount: Click here

My annual rate of return: 7.8% (After fees but before taxes)

My Kuflink Review: What You Need To Know

Thumbs Up

- Loans secured by UK property

- New loan flow is good

- Transparent loan information. Each loan is well documented and explained / property valuation reports are easily accessible

- Good loan repayment history

- Manual and auto-invest options. Auto-invest offers a lower average LTV

- You can cancel your loan bids prior to loan going live

- 14 day cooling-off period for new customers

- Low £ minimums for reinvestment of interest payments

- Family-owned business with extensive lending experience

- Has a charitable foundation to help local community

Thumbs Down

- Kuflink is under FCA restrictions and cannot onboard new investors and has been instructed to close it’s auto lend product

- Questions about its future operations

- Auto-invest interest payments are made once annually

- Blended default rates were over 16% in 2024

- Borrower loan interest rates aren’t shown

- 1% loan seller fee on secondary market

- Can only buy secondary market loans in fixed sums

Read more below in my exclusive Kuflink review.

Alternative Companies

Crowdproperty, Proplend

Kuflink Review: My experiences so far…

I made my first investment through Kuflink in April 2018. I watched their loan offerings and repayment history for over a year prior to investing. In every form of lending business, defaults are inevitable and while Kuflink’s default rates have been higher in 2024, they appears to have good recovery results.

In August 2018, I hopped on the train to Gravesend to visit Kuflink’s offices and meet the staff for the first time. I was particularly impressed with the staff’s dedication and passion, the strong foundation of company culture and the founders’ charitable hearts. You can even pop into their office for ice cream!

What Is Kuflink?

Kuflink is a peer to peer lending company that offers lenders opportunities to invest in short-term, 3 to 12 month bridging loans. All loans are secured by property should the borrower default. Kuflink offers both manual (non ISA account) and auto-investing (ISA and regular accounts) accounts with varying return rates. Kuflink invests its own funds alongside lenders’ so their interests should be aligned with lenders.

How Can I Contact Kuflink?

www.kuflink.com

Email: hello@kuflink.com

UK Tel: 01474 334499

When Did Kuflink Launch?

May 2016

Are They Regulated?

Yes, by the Financial Conduct Authority #724890 under full permissions granted April 27th, 2017. Investments made through Kuflink are not covered under the FSCS (Financial Services Compensation Scheme). FCA regulation is nothing like the FSCS, which covers consumers when they deposit money in banks. The FCA reports to the UK government and has the ability to pursue criminal action against companies that violate its standards and codes of conduct.

Who Can Open An Account?

Any person 18 years or older who has a UK bank account and can pass the verification checks. If you live in a foreign country and you have a UK bank account, you can apply.

Does Kuflink Allow Corporate Accounts?

Yes, you can open an account under a corporation. You just need to provide the necessary documentation. You can read more here.

What’s The Signup Process Like?

Kuflink runs the usual KYC anti-money laundering checks. You can open an account in five minutes by providing a name and email address and then uploading a copy of your passport or drivers license. I found the verification and account opening process to be quick and simple. Overseas investors are welcome but they must have a UK bank account.

I applied and was approved in three minutes. I filled out the information online, uploaded my passport photo and verified my identity using an SMS link and a selfie photo. Kudos to Kuflink for making the process so easy.

What’s The Minimum Investment?

New Investor Minimum Investment: £100 into one single loan or Auto invest

How Are Deposits Made?

Via bank transfer or maximum £9,999 via a debit card

Does Kuflink Offer An Innovative Finance ISA (IFISA)?

Kuflink offers an IFISA wrapper that can be used only for the auto-invest product and certain self select loans.

What Types Of Lending Products And Accounts Does Kuflink Offer?

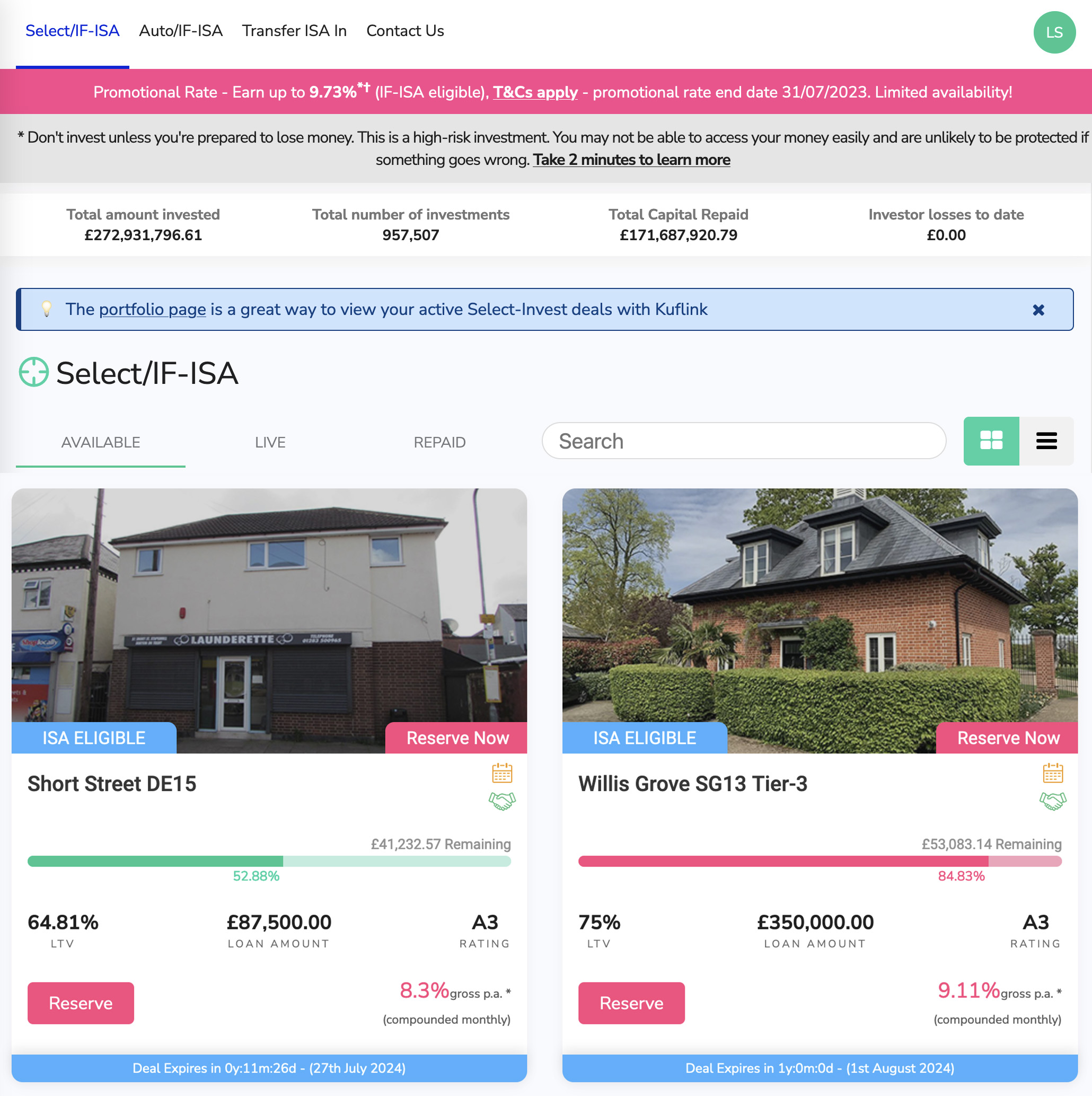

Select-Invest: This manual lending product allows lenders to choose which loans they would like to invest in. You can now use an ISA wrapper to manually invest for certain loans which is a nice addition. Here’s what the self-invest dashboard looks like:

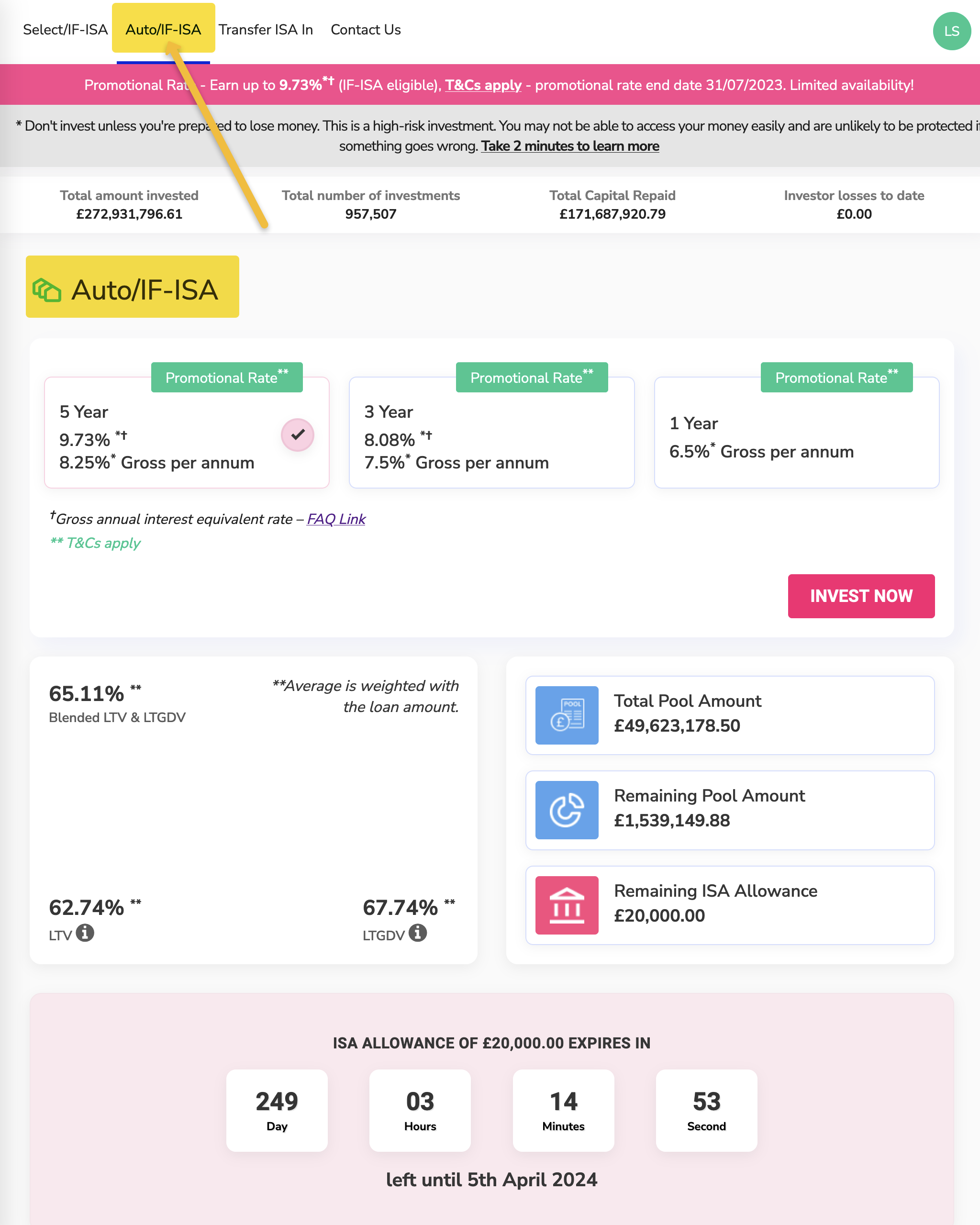

Auto-Invest: Terms of 12, 36 and 60 months are offered. Your investment is automatically diversified across a portfolio of loans. Each term pays a different return rate. Investing is as easy as depositing money, picking your term and choosing your investment amount. Here’s what the auto-invest dashboard looks like:

Auto-Invest: Terms of 12, 36 and 60 months are offered. Your investment is automatically diversified across a portfolio of loans. Each term pays a different return rate. Investing is as easy as depositing money, picking your term and choosing your investment amount. Here’s what the auto-invest dashboard looks like:

How Much Gross Annual Interest Are Lenders’ Expected To Be Paid?

Rates vary but Manual invest ranges from 7- 9.5%

The Auto invest product has been discountinued per the FCA but rates used to be up to 10%.

(These rates include a promotional interest rate bump which can end anytime)

How Long Are The Investment Terms?

Manual invest: 3 to 12 month loan terms

Auto-invest: 12, 36 or 60 month terms (no longer available)

Is Interest Paid Immediately Or When the Loan Starts?

When you manual invest, loans are offered prior to launch. When you pledge money, daily interest accrues and is then paid as cashback the day the loan goes live.

When Is Interest Paid?

Self select invest interest is paid on the first business day of the month.

Auto-invest interest is paid annually on the anniversary of your investment.

Is There A Secondary Market

Yes and it allows lenders’ to buy and sell loans with no premiums or discounts. If you sell a loan you will be charged a 1% fee.

Am I Lending To Kuflink Or The Borrower?

Kuflink is a true peer to peer lending company so you’re loaning money directly to borrowers rather than to Kuflink the company.

What Are The Fees?

1% fee of total amount for selling a loan on the secondary market

How Much Time Will I Need To Spend Managing My Investments?

If you chose to manual lend and are considering investing any substantial amount of money, you should be prepared to perform your own risk due diligence to verify property valuations and other information. The amount of time needed to research loans will come down to personal preference. Most inexperienced retail investors may struggle to evaluate this information.

The discontinued auto-invest product required no time management.

What Security Does Kuflink Lend Against?

Kuflink secures each loan by placing first or second charges on the property that is being borrowed against. If the borrower defaults, a first charge on a property can be used to attempt to recover capital and interest. Second charges are far more troublesome in default recovery, especially when property loan to values are higher. Kuflink keeps property loan-to-values below 75% but they can be much lower depending on the loan.

What Are The Loan Default / Loss Rates?

Kuflink provides fully transparent default and recovery stats. You can check the latest default stats here and you can also download a full historical track record spreadsheet.

What Are The Main Risks?

Company Failure: This is a risk with every peer to peer lending company, especially ones with smaller loan books. If their business model fails, investors could lose all of their investment though it’s more likely they would lose some of their investment.

Economic downturn: Kuflink is now experiencing a severe economic downtown due to Covid-19. This will cause more borrowers to default so it will be essential to see how Kuflink handles default recovery.

Valuation issues: Some peer to peer companies have struggled to obtain accurate RICS property valuations. If the valuations are incorrect and the property defaults, there may be a shortfall in recovery amounts.

Borrower defaults: If borrowers stop making loan payments, a default process is put into motion. Property default recovery can be lengthy, sometimes running into years.

Is There A Provision Fund?

Technically Kuflink doesn’t have a provision fund but it does take the first 5% loss of every loan it offers. This money is provided by Kuflink Group PLC. This first loss offer is a unique level of protection offered to cover peer to peer lenders but is only as good as Kuflink’s ability to cover the losses. Personally, I think the word “guarantee” needs to be removed. You can read more on my thoughts about this later in the review.

What Happens If Kuflink Goes Out Of Business?

Kuflink is required by the FCA (Financial Conduct Authority) to have a sufficient wind-down plan in place. If Kuflink were to go out of business, there is an agreement with a third-party service provider to manage all loan agreements so interest payments are maintained.

If insolvency occurred, an administration company would work on behalf of the creditors (people owed money by Kuflink) and customers (loan borrowers) to recover as much money as possible. It’s important to know that we (peer to peer lenders) are not considered creditors.

Winding down a loan book would involve fees that are taken from any recovered money so lenders would likely see a loss of capital if Kuflink were to close its doors. This is part of the risk of peer to peer lending.

Though unlikely, there are many unknowns that can occur when a peer to peer company goes out of business. As with any investment, be aware that your capital is at risk.

You can read more about Kuflink’s wind-down plan here.

KUFLINK THUMBS UP

Kuflink’s Founders Have Extensive Property lending Experience

Prior to launching Kuflink in 2016, its founders had extensive experience as property investors and lenders through the Alpha Bridging brand which was operational since 2011.

Loans Secured By Property

All of Kuflink’s loans are secured by property so if the borrower defaults, the capital and interest can try to be recovered by selling the property.

5% First Loss

Kuflink used to take the first 5% loss for all loans it held a stake in. This lowered lender risk as long as Kuflink is financially able to stand by this guarantee should the worst happen. Kuflink no longer takes a 5% first loss stake in any loans.

Secondary Market

Kuflink’s resale market allows lenders’ to buy and sell loans. There are no premiums or discounts.

I recently tested the market with a small resale amount. I was able to sell my loan part within two hours.

The secondary market isn’t the easiest feature to find, so here’s how:

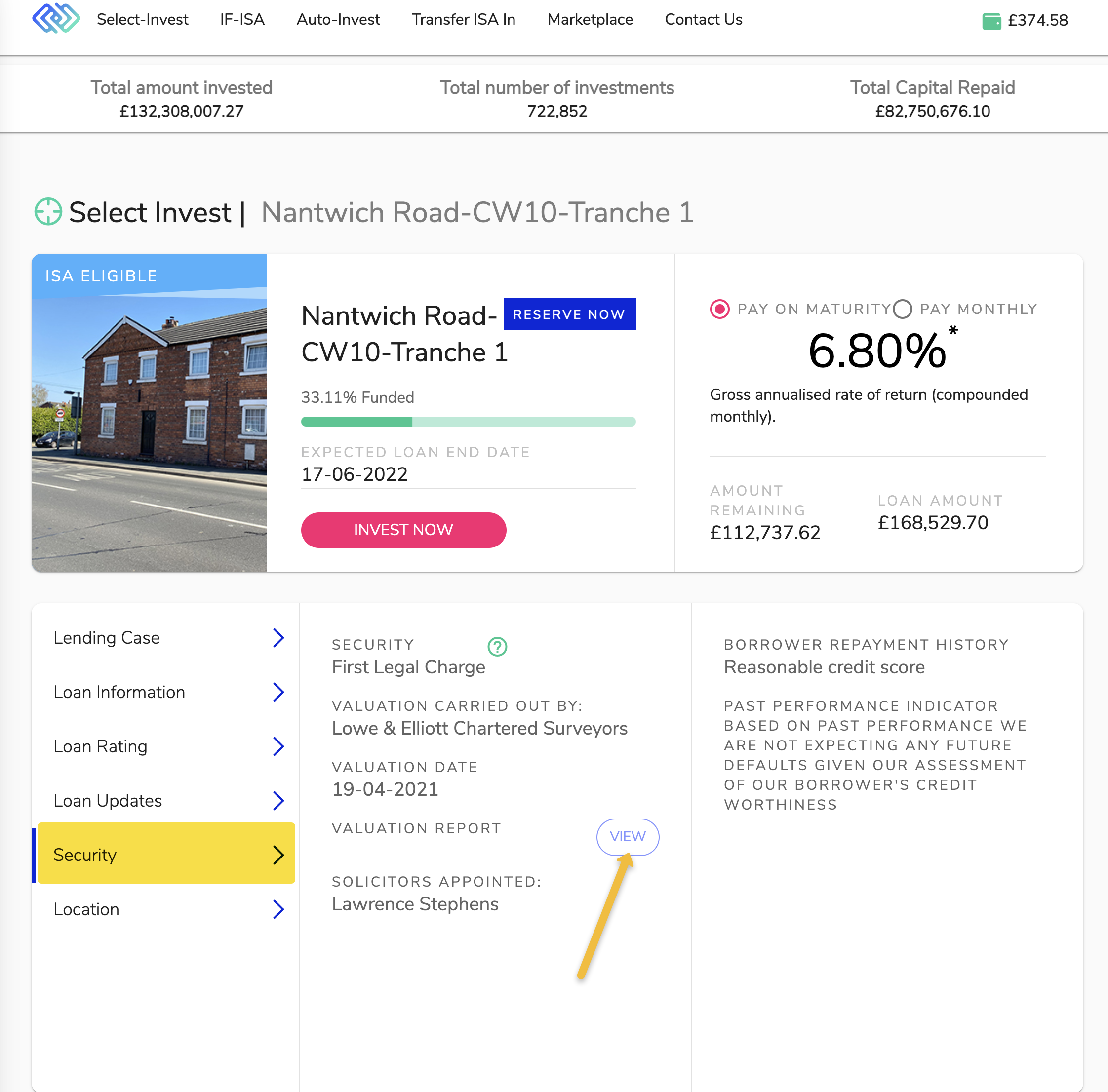

The one feature I would like to see adjusted is the ability for the loan buyer to choose the amount of the loan part they would like to buy. For example, on the above graphic, you can see if you wanted to buy the Warwick Crescent loan you would be forced to by a £5,000 chunk rather than choosing how much of the loan you wanted to buy.

Well Documented Loan Information And Valuation Reports

I’m impressed with how much accessible information Kuflink provides on each offered loan. This includes valuations, a loan rating from A to C, loan-to-value percentage, borrower credit health, Kuflink’s loan stake size, and easy to find RICS valuations:

Not every peer to peer lending company provides RICS valuation reports on there website so this is a nice feature for those wanting to do their own due diligence.

Many Loans Repaid

Kuflink has an extensive loan repayment history showing it has a solid repayment track record.

Cancel Your Loan Allocation Prior To Launch

This handy feature allows you to change your mind if you pledge money to a loan you decide you don’t want to proceed forward on. Simply contact Kuflink and they will remove your pledge prior to the loan being fully funded.

14 Day Cooling Off Period For New Customers

If you transfer money as a new customer, pledge money to loans and decide Kuflink’s not for you, Kuflink will allow you to cancel your loans and withdraw your money within 14 days.

Low £ Minimums For Reinvestment Of Interest Payments

If you just want to dabble with a small starting investment amount on Kuflink, you’ll be glad to know loans have low investment minimums. The minimum investment must be enough to earn 1p of interest each month. The closer to month end, the more you must invest to earn minimum interest, hence the higher the minimum investment becomes. Each loans information page clearly displays the minimum needed:

You can start investing in the auto product with £100.

KUFLINK THUMBS DOWN:

FCA Restrictions

Kuflink is under FCA restrictions and cannot onboard new investors and has been instructed to close it’s auto lend product. This brings into question why these restrictions were placed and how stable Kuflink’s business is? Will report back on this situation as more info is discovered.

Borrower Interest Rates Aren’t Shown

Kuflink used to show the borrowers loan interest rate but this was removed from the loan information. It’s important for this information to be easily seen so investors can evaluate risk.

Auto-Invest Payments Are Made Annually

When you invest in Kuflink’s auto-invest products, you will only receive one payment on your annual investment anniversary. This won’t be ideal for those looking for regular income payments.

Can’t Buy Pieces Of Secondary Market Loans

Secondary market loans are difficult to come across since investor demand is much higher than loan

Selling Fee on Secondary Market

I’m very happy to see the launch of Kuflink’s secondary market. If I could change one thing it would be to remove the 1% sales fee that is charged to the loan seller. I think secondary market fees can discourage people from selling loans, therefore slowing down secondary markets.

Auto-Invest Shorter Term Return Rates Are Lower Than Some Self-Select Loans

If you compare interest rate returns, the 12-month auto investment rate versus select is a bit low for my liking. Auto invest does take the hassle out of choosing your own loans and provides easy diversification but you’ll lose about 1.5% – 2% interest for the convenience. easy t if you tie up your money for years, there are currently no exit options.

My Strategy

I monitored Kuflink’s loan offerings for a while before I started investing. I used to manually pick loans and switched to their one year auto invest product, mainly due to lack of time to pick loans. The auto-lend product has been stopped due to FCA restrictions. I’ve greatly reduced my Kuflink holdings and and will not invest further until further clarification on the FCA situation is received.

Kuflink Review Conclusion

I’ve visited the Kuflink offices several times and I felt the company offered a solid peer to peer lending product secured by properties at reasonable loan-to-values. Kuflink’s team are very experienced and Kuflink’s return rates are competitive. Unfortunately, things changed with the departure of some key Kulfink people and the FCA restrictions leaving unanswered questions.

Until those questions are answered, I would proceed cautiously before investing into Kuflink’s loans.

Sign up for a Kuflink account. (Read the terms and conditions here. When you open an account through my website, it helps me to continue to operate and offer new reviews).

If you enjoyed this Kuflink review and want to know more, click here and receive my complimentary Top 5 Peer to Peer Lending Sites Report.

I love feedback, so if you find any errors or omissions in this Kuflink review or have any improvement suggestions, I invite you to contact me and be a part of contributing to this website.

Disclaimers: I have not paid to write my reviews and I’m not employed by any of the companies I write about. In most cases, I have invested or continue to invest my own money through these companies. In order to keep the website financially viable, the sign-up links on this website are referral links and I do accept advertising in the form of banner ads. This advertising in no way influences my reviews and opinions. When you sign up for an account through my website, in some cases I receive a referral fee directly from the companies, at no cost to you. Your support enables me to continue to operate the Financial Thing website. You can read more about my referral links and banner advertising here.

** This Kuflink review is for information purposes only. This information is not financial advice and has been prepared without taking your objectives, financial situation or needs into account. You should consider its appropriateness for your circumstances. All investing carries risks. Opinions expressed in this review are opinions based on my own personal experiences. The FSCS does not cover peer to peer lending and your capital is at risk. Please don’t invest more than you can afford to lose. **