“I had 3 financial advisors when in business. The first two were good. The last one – we had to part company – particularly when he would not agree to waive his commission after losing me money. A few years later ZOPA came along. From that point on, I never looked back, I always out-perform all my previous financial advisors – even the good ones. And of course, I have never used a financial advisor again.”

– Reg. B, Financial thing reader

I love receiving emails from readers like Reg. An educated investor is one who can save tens of thousands of pounds / dollars in financial planning fees over his lifetime.

Let me start by saying this article isn’t intended to bash financial planning advisors. I think certain people need advisors; I did at one point in my life. This article was written to highlight why you don’t necessarily need a financial advisor and how you can do your own financial planning and DIY investing.

I’ve written it time and time again. Fees are the killer of investment returns. Let’s start by looking at how much a “tiny” 0.5% advisor annual fee can cost you over a period of your investing lifetime. Here’s the fee on a £150,000 investment:

| Investment Amount Left 30 Years | Return % | End Amount | 0.5% Fee Cost |

| £150,000 (With Advisor) | 6.5% | £1,048,769 | £168,645 |

| £150,000 (No Advisor) | 7% | £1,217,414 | |

Wait, that can’t be right can it? Did financial advisor fees really cost me over £168,000? Yes that’s exactly right; you can verify the numbers using a compound interest calculator. The numbers become even more astonishing when you increase the investment amount to £300,000:

| Investment Amount Left 30 Years | Return % | End Amount | 0.5% Fee Cost |

| £300,000 (With Advisor) | 6.5% | £2,097,539 | £337,410 |

| £300,000 (No Advisor) | 7% | £2,434,949 | |

Fee cost saving is the number one reason why you should be doing your own financial planning.

“Just remember, the person (IFA) you’re talking to, your fees are their income”

– Warren buffet

CNBC May 2017

Financial planning and DIY investing seems complicated, but it can be really simple once it’s simply explained. The problem with the investment world is it’s designed to be complicated, similar to the way car dealerships are designed to annoy you into giving in and paying the price they want you to pay. My friend John recently went into a Mazda dealership with a £19,000 cheque in his pocket, determined not to pay a penny more for his new Mazda 3. After five hours of tiring back and forth negotiation, John paid £21,000 for his new car. This is a common technique of profitable car dealerships. Keep the customer hanging around until they can no longer endure the negotiation.

The investment world is no different. Consumers are faced with tens of thousands of investment products. The average consumer becomes so overwhelmed by choice that they see no other option than investing through an advisor. Who can blame the consumers for following this traditional path?

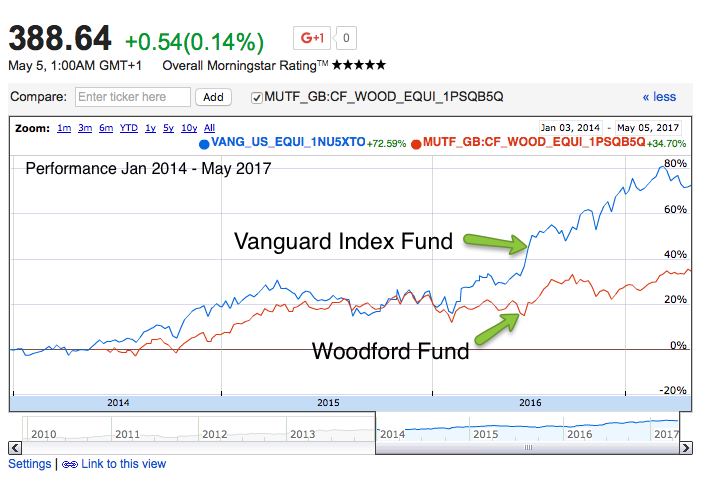

In January 2014, I met with a financial advisor because I had no idea how to invest. Bob the advisor suggested I invest in the Woodford Equity Income Fund, or a “staple of British funds” as Bob liked to call it. I invested in said fund and Bob charged me a 0.50% annual fee for the privilege. The fund annual fee was advertised at 0.75% in the brochure; but wait, there’s more….fees:

After further digging I discovered the Woodford Fund fee was actually 0.84% per year. This sneaky practice of hiding fees is abused by nearly every managed unit trust. In fact most funds have hidden costs far greater than the Woodford Fund. These costs come from the high stock turnover generated by trading fees and capital gains taxes. You, the fund investor, pays the fees. So in fact the Woodford Fund was actually costing me a whopping 1.34% annually when I added the financial advisors fee. No thanks.

In 2014, I read John Bogle’s Little Book of Common Sense Investing and figured out the Woodford Fund fees along with the financial advisor fee were going to be very damaging long term. I promptly sold all but £500 of my Woodford Fund and purchased index trackers. I know what you’re thinking, “Laurence, why did you keep £500’s worth?”

Just for fun, I wanted to keep £500 of the Woodford Fund to track performance over 30 years. Until Mr. Woodford invents a stock picking crystal ball….

..the Woodford Fund cannot win over the long run.

If I had stuck with my financial advisors advice, here is how I would have fared:

The Woodford Fund underperformed the S&P 500 Fund by almost 38% over three years. I later went back to Bob the advisor and asked him why he hadn’t offered me a nice simple tracker fund. Bob informed me that index trackers don’t perform well in volatile markets, and that it’s much better to have an active fund manager buying and selling shares on your behalf.

Bob was wrong.

So Who Needs A Financial Advisor?

There are a few cases where financial advisors are beneficial.

It is far better to invest through a financial advisor than not to invest at all. Some people lack the confidence to make financial decisions and could find themselves sitting on the fence forever. An advisor can be a good way to help push you off that investing high diving board when you’re afraid to jump.

Once you are invested, you can do your research and move on from the advisor when you feel comfortable. Or at the very least, invest some of your own money alongside the advisor and see which investments are performing better. My own mother uses a financial advisor for part of her portfolio for comparison purposes.

Also, some financial advisors are proficient in tax planning. This type of advisor can be a good compliment to your own investment strategy. No one should pay more to the taxman than they have to.

Other people who might use an advisor are happy with the returns they achieve through and feel like the advisor provides them a certain level of comfort. I have a friend who is a millionaire and the extra 1.5% annual fee doesn’t bother him at all. He also likes the fact that when something goes wrong, he can call and yell at his advisor. Strange logic but it works for him.

Finally, occasionally, financial advisors have access to private investment opportunities that a DIY investor might not have. Examples are property developments and business investing. I have a friend who buys businesses that are performing poorly and turns them into profitable ventures. Sometimes he sources investment capital through accountants and financial advisors.

So how does one go about becoming a DIY investor?

My Four Step Process To Doing Your Own Financial Planning & Investing

Step One: Analyse your portfolio and write down the annual fees. Don’t forget to add your advisor fee and any brokerage platform fees.

Step Two: Look at index trackers. Vanguard’s US Equity S&P 500 Index Tracker and Vanguard’s Global Bond Index are my go-to funds. Notice the low fees and use this compound interest calculator to see how much these lower fees will earn you over various amounts of years. You can read this article on why I like these two funds.

Step Three: Buy your trackers using a low cost brokerage such as Halifax / iWeb or buy directly from Vanguard.

Step Four: Fire your financial advisor (in a kind way of course).

Seems way too simple right? It does because it is.

Happy DIY investing!

“Costs really matter in investments…If returns are going to be seven or eight percent and you’re paying one percent for fees, that makes an enormous difference in how much money you’re going to have in retirement.”

– warren buffet

cnbc may 2017