The Best Tracker Funds

** Updated March 19th, 2025**

![]() Join the Financial Thing VIP Investment Group and chat with myself and other like-minded investors

Join the Financial Thing VIP Investment Group and chat with myself and other like-minded investors

__

Let’s get right to the point. John Bogle’s book “The Little Book of Common Sense Investing: The Only Way to Guarantee Your Fair Share of Stock Market Returns” was the most impactful investing book I’ve ever read.

The book explains why buying index tracker funds over the long term is far better than stock picking or investing in managed unit trusts and mutual funds. This is true for all levels of investment experience.

I like looking into my crystal ball and stock picking (gambling) as much as the next person, but there’s too much evidence that most investors and professionals won’t beat the market over a long period of time, myself included.

As my close friend who runs a Wall Street hedge fund told me, “listen to me closely, and this is coming from a professional who has been in the industry for 20+ years, stocks are fugazi, there is no rhyme or reason as to why they go up and down on any given day and no one can predict stock movement”.

Stock picking can make you feel like a genius during a bull market when prices are going up. IF you can correctly identify which sectors are profitable, and which stocks within those sectors are profitable. For example, up until the end of February 2021, technology stocks were raging upwards. Then in early March 2021, tech stocks plummeted and oil and energy stocks erupted. Then in mid 2023, the tech sector raged upwards. Then in. March 2025, the stock sky fell again and “safer” assets such as gold and silver became popular.

Timing these cyclical stock moves is nearly impossible and requires lots of research and luck. The issue is when stock prices are dropping, emotions get involved and bad timing decisions can cost you money. Amateur investors tend to panic sell when prices are plummeting and buy when they are rising. The opposite of what they should be doing.

(I’m currently recording a video series on stock picking where I pony up £5,500 of my own cash and try to beat the returns of my index trackers by stock picking. (You can watch my weekly livestream for portfolio updates here).

Forget what your grandad told you. You know, the advice about letting a financial adviser build you a unit trust or share portfolio filled Threadneedle, Invesco, Artemis, Shell, Marks & Spencer, Rolls Royce and Lloyds Bank. You can’t blame grandad’s advice because that is what his trusted financial adviser told him to do; the same adviser who was paid handsomely from unit trust and mutual fund front and back end incentives (also known as loads), trading commissions, and annual trailing commissions.

I’m not here to bash financial advisers. I’d rather see someone with zero investment knowledge sensibly invest through an adviser than not invest all. But you’re not one of the people with zero knowledge. You’re a Financial Thing reader so you don’t have to fall into a fee-paying adviser trap.

While I am starting to understand stock movements aren’t always logical and price reactions in today’s world don’t correlate with the current financial environment, one should still include them as part of a diversified investment strategy.

There is a time-tested investment strategy that greatly reduces risk, prevents emotional selling, and reduces fees while providing you with a fair chance of healthy returns.

Choose the best tracker funds.

“There seems to be some perverse human characteristic that likes to make easy things difficult.”

– Warren Buffett

Warren Buffet’s words are extremely insightful. Humans love to complicate things, especially when it comes to investing. The investing world is complicated by design after all. In the UK, there are over 2,000 different unit trusts and in the USA, over 7,500 mutual funds.

What’s even better news is this passive index fund strategy can be used during the worst economic times of instability because they remove the emotional tendencies that stock pickers battle. You are less likely to sell a single fund you own than you are to sell pieces of a stock portfolio that is in the red.

So why choose the best tracker funds?

Three reasons.

1. Index tracker funds have low fees,

2. They tend to outperform most managed funds over a very long period of time

3. They are tax-efficient.

Index trackers won’t provide with you the +50% annual or even daily returns gambling on a single “meme” stock might, but you can rest easy investing in an index tracker knowing the decisions making stresses can be removed.

I once spoke with a financial adviser who argued I was wrong about tracker funds and told me that you get what you pay for with actively managed funds. I questioned exactly what I was getting for all those active management fees and fund manager salaries I was paying and eventually told him I respectfully disagreed to which he responded, “Well, people don’t want tracker funds, they are too boring”.

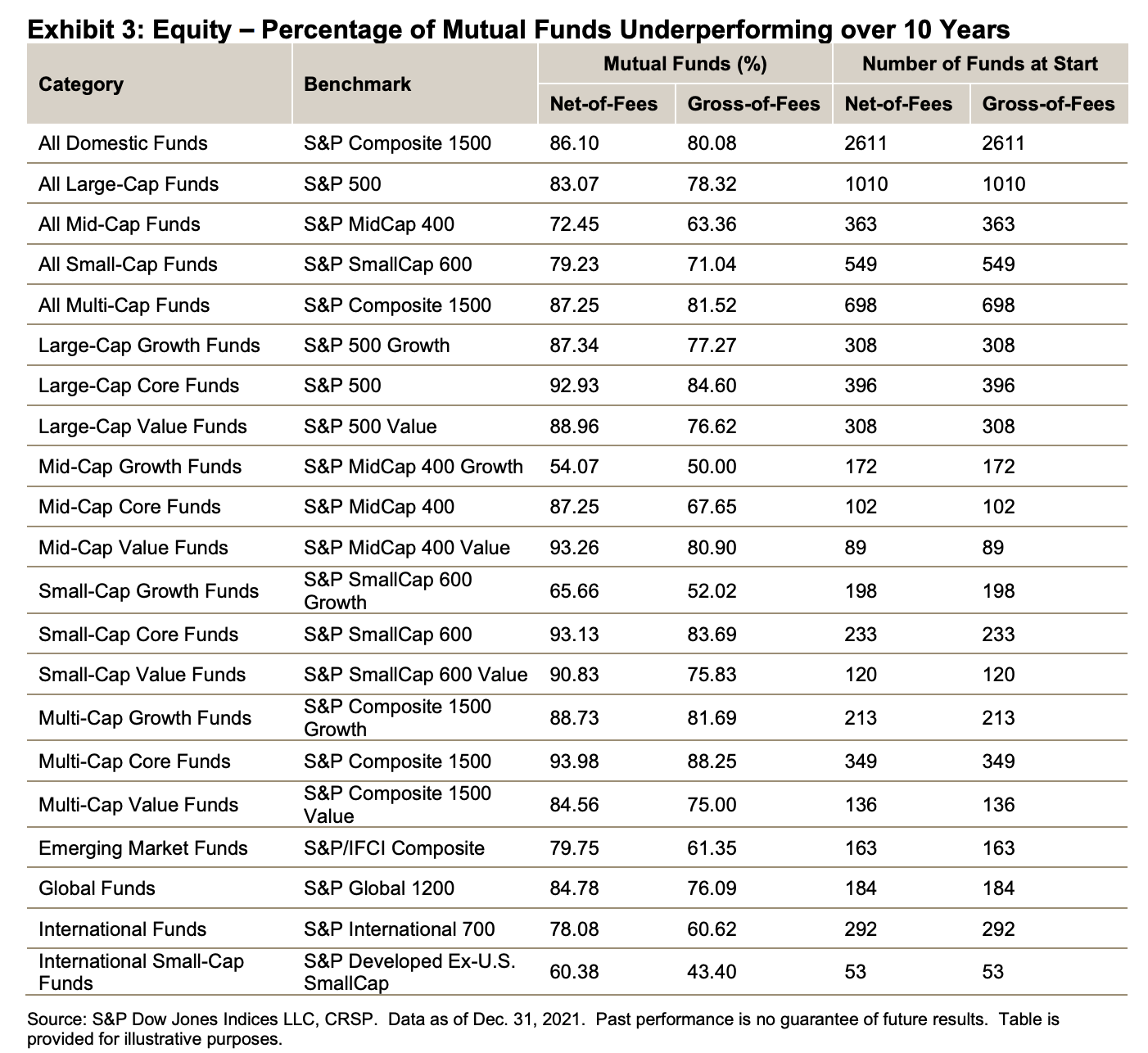

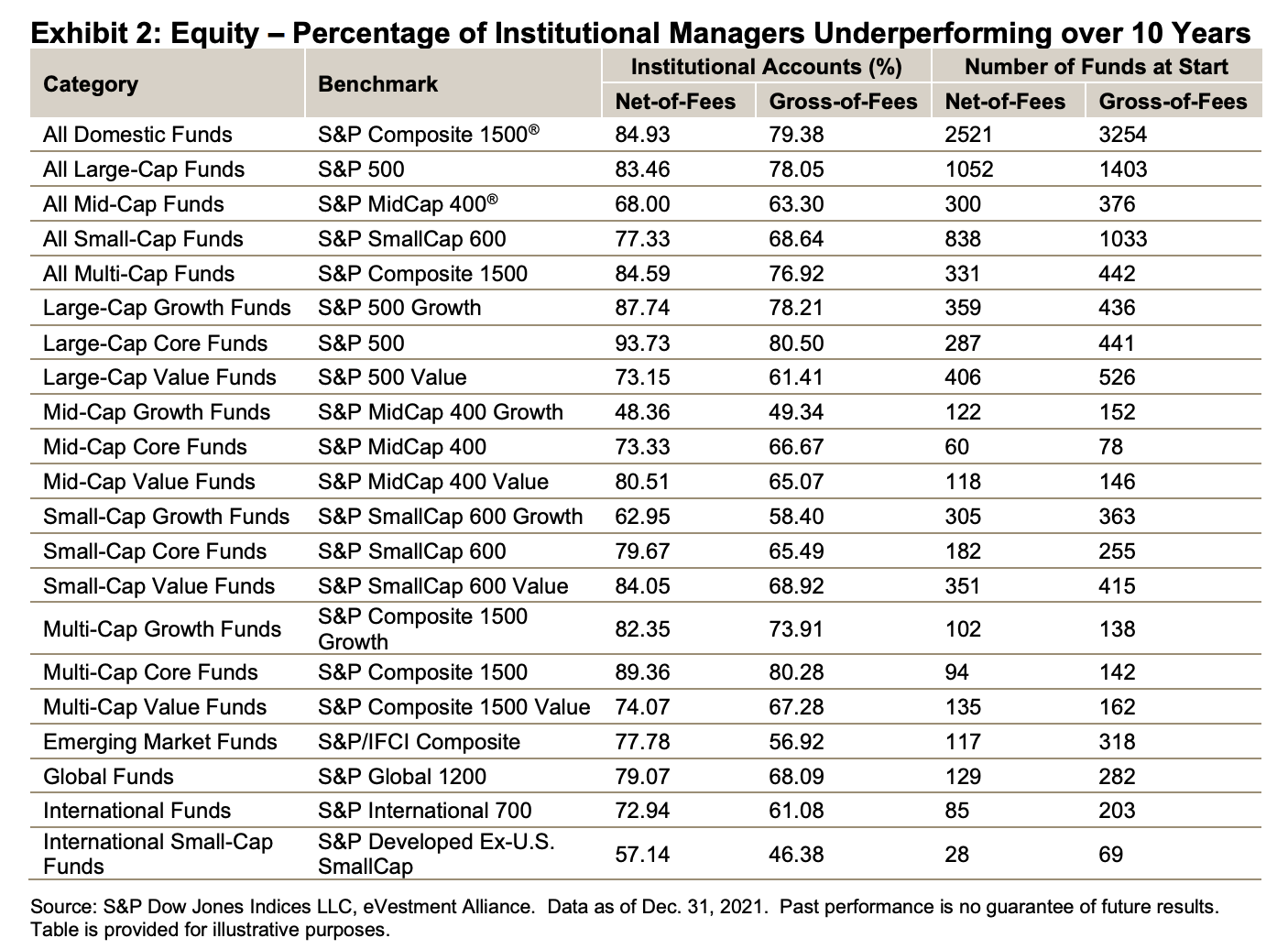

Want proof of how badly actively managed funds performed versus their benchmarks?

The S&P Dow Jones Indices releases data throughout the year.

Here are some staggering fund facts from their 2022 mid year and 2021 yearly reports:

- Over the last 10 years, 83% of both large-cap institutional managed accounts and large-cap mutual fund managers underperformed the S&P 500

- Pricey active large-cap funds are doomed to failure: Just 6% of these funds beat the S&P500

(source)

Managed funds continue to underperform passive investing yet many investors continue to let these “professionals” invest their money.

Even my Trading 212 portfolio has obliterated most managed funds by tripling in value over 12 months and I am far from a trading professional. This was mainly due to blind luck and not skill by the way.

Some large U.S pensions funds are waking up to the stark reality that active fund managers rely heavily on luck. The California Public Employees Retirement System has moved billions of $’s from active funds to passive funds.

Any financial adviser who advises you to buy actively managed funds might be trying to separate you from your money by way of incentive commissions, management and trading fees. There are countless professional investment fund managers, some of who are paid astronomical annual salaries (some over £1 billion), who have lost money year after year and most managed investment funds have struggled to beat their index benchmarks.

Some actively managed fund advisers have made disastrous stock-picking choices that drove their fund prices into the ground. Neil Woodford would be one such example. Ingenious branding and expensive advertising campaigns persuade new customers these managed funds will outperform the broad market S&P 500 index. In Woodford’s case, this turned out to be snake oil as Woodford’s fund fell into administration along with billions of £’s of investors’ money due to poor investments made by the money managers.

I actually owned some of Woodford’s fund as I was testing the performance against my index trackers. Although I didn’t own much, my timing was extremely lucky as I sold in 2016 and 2018 due to poor performance:

Did you know there are approximately 2000 unit trust funds available to UK investors and 7,500 mutual funds in the USA with more being added daily?

With a small percentage of these funds outperforming the S&P Total Market index over long time periods (talking decades here), how could anyone pick the correct funds, let alone understand them? Another issue is one fund might perform gloriously one year while the following year, it could fall flat on its face due to the fund manager picking the wrong shares.

Artemis’s actively managed US Select Fund is a great example of an actively managed fund that underperformed the S&P 500. This fund gained 29.1% in 2019 while the S&P 500 index gained 33%. The 4% difference in gains might not seem like much but compounded over 20 years, this 4% annual difference would cost you a staggering £329,651!

Do you know some of the mega-funds hold the same investments but charge different fees? For decades, stock funds were shrouded in hidden fee mystery until the Government finally said enough and forced fund companies to be more fee transparent.

The financial services world is complicated for a reason because if it weren’t, very few people would need financial services.

Previously, I wrote an article about why you should avoid checking share prices and avoid buying single company stocks because it’s too risky.

Look, I love picking single stocks but I also spend countless hours researching the stocks I buy, and sometimes, I make bad picks. For example one of my previous stocks, Aurora Cannabis, fell 25% and I sold at a loss. One stock I chose, Norseman Gold, actually went to zero when the company went bankrupt. Yes, stocks can go to zero.

If you want to fulfill your gambling desires and have a punt on single stocks, make sure you only allocate a manageable percentage of your entire investment allocation. 10% maximum.

In a bull market, even an amateur stock picker can look like a genius. But in bear or sideways stock markets, you shouldn’t stock pick because you can get crushed by bad trades. Remember when you are buying stock, you are trading against another person (the seller) who is likely a professional and knows more than you. One bad stock trade can wipe out months or years of gains.

So if not single stocks, then what?

The answer is to buy the best tracker funds, also known as index tracker funds. They are simple, have historically outperformed most actively managed funds long-term and most importantly, they have low fees, low turnover and are tax-efficient because of the infrequent trading that lowers capital gains taxes.

When you begin looking for the best tracker funds, the financial services industry will try to dissuade and confuse you by offering a myriad of options designed to have you running back to your trusty financial adviser. No one needs a financial adviser to buy index trackers.

So how do you know which are the best tracker funds to buy?

Firstly look for low cost and simplicity. There are many types of index trackers so it’s best to choose something you’re comfortable with and that you understand.

Personally, my best tracker funds list is very short as my entire tracker portfolio contains just one or two funds:

Best Tracker Funds For Equties #1

1. Vanguard US Equity Tracker Index Fund

- June 23rd, 2009 Launch Price: £100 (accumulation)

- March 18th 2025 Price: £960 (accumulation), £780 (income)

- Annual Dividend Yield: 0.96% (gross, yield changes often)

- Fund Type: Passive, accumulation or income

- Annual Fund Ongoing Charge (OCF): 0.10%

- Transaction Cost: 0.02% (paid from inside the fund)

- Purchase Fee: 0% (if purchased on Vanguard’s website)

- Exit Fee: 0%

- Total Fees through Vanguard’s website:

- £32k or less account balance: £48 per year account fee + annual fund fee (0.15%) £32k+ account balance: 0.15% per year (max of £375 per year) + annual fund fee (0.15%)

- Market Allocation: 100% U.S. stocks

- Risk Level: 5/7

- Total Stocks In Funds: 3550

- Benchmark: S&P Total Market Index

- ISA Eligible

- Where To Buy: Vanguard UK or most trading platforms

- Min Investment: £500 directly from Vanguard, £100 minimum for monthly direct debit, Min amounts vary on other brokerage platforms.

This Vanguard U.S. Equity Index Fund tops my list of the best tracker funds because it holds a wide array of company stocks, everything from behemoths such as Apple and Amazon, staples such as Visa and General Motors, and smaller companies such as Dolby and Ralph Lauren. The fund tracks the S&P Total Market Index and includes stocks from the S&P500, Dow Jones and the Nasdaq. In other words, the fund tracks the broad equity market including large, mid, small and micro-cap stocks.

The fund purchases stocks in a weighted format. For example, the largest weighted stocks are Apple, Microsoft, Amazon, Facebook and Tesla make up around 18% to 20% of the whole index, so the tracker fund owns the same percentage of its holdings in those 5 giant companies. This continues all the way down to the smallest company which represents 0.00001% of the index.

This type of fund benefits from diversification and company growth and you receive a small dividend yield. You can take the dividend yield as a cash payment (Income Fund) or you can reinvest dividends (Accumulation Fund). Because dividend yields are low, I would advise buying the accumulation fund to take advantage of the power of compounding interest, unless of course, you need the income. The income though is relatively small since the dividend is low.

Vanguard’s US Equity tracker fund seeks to track the indexes passively and will perform as the markets perform.

The beauty of passive index trackers versus managed funds is that you don’t have to gamble on choosing one of the few managed funds that outperforms the indexes. Take Neil Woodford’s rise and fall as a lesson in managed fund avoidance. Instead of trying to pick winners from thousands of unit trusts or mutual funds, pick one tracker fund that owns thousands of stocks in proven companies such as Apple, Microsoft, Google and Visa.

The Vanguard fund is valued in U.S. dollars so you do have some currency exchange rate risk, but the pound has historically favoured well against the dollar and the risk averages out over time. Vanguard has an excellent article explaining currency risk here.

You can also buy a similar Vanguard S&P500 fund (VUAG) through Investengine which under their DIY option which costs zero to purchase. Sign up here for a nice Welcome Bonus!

So why not invest in a FTSE 100 index tracker?

Historically, the FTSE 100 index has grossly underperformed the S&P 500 index. The FTSE 100 is too small and isn’t diverse. At one time, BP, Shell and HSBC comprised almost 25% of the FTSE 100.

The FTSE 100 has historically underperformed the USA’s S&P 500 by large percentages:

Regarding stock market returns, all we can look at is history and while history is no indicator of the future, you can see how historically the FTSE 100 index (blue line) has grossly under performed America’s S&P 500 index (red line). That being said, some people are only comfortable buying UK investment products, so always do what is right for you.

What about a global index tracker?

Choosing Fidelity’s Global Tracker Fund would be my second equity tracker choice but the Global Funds have historically under performed the US tracker’s by about 3% per year since 2012:

I prefer the Fidelity Global index tracker because of the diversity as the fund invests in 1400 stocks versus Vanguard’s version which only invests in 200 stocks. Fidelity’s global tracker invests in about 72% of U.S markets so you’ll get exposure to both US and global stocks.

Best Tracker Funds For Bonds #2

2. Vanguard Global Bond Index Fund Hedged

- June 23rd, 2009 Launch Price: £100

- March 18th 2025 price: £153 (accumulation), £120 (income)

- Annual Dividend Yield: 2.85% paid quarterly (Gross)

- Fund Type: Passive, accumulation or income

- Fund Annual Fee: 0.15% (if purchased through Vanguard)

- Annual Transaction Cost: 0.14% (paid from inside the fund)

- Entry / Exit Fee: 0%

- Total Fees through Vanguard’s website: £32k or less account balance: £48 per year account fee + annual fund fee (0.15%) £32k+ account balance: 0.15% per year (max of £375 per year) + annual fund fee (0.15%)

- Market Allocation: 100% international government and corporate bonds

- Risk Level: 4/7

- Total Bonds In Fund: 12,780+

- Benchmark: Bloomberg Barclays Global Aggregate Float Adjusted Index Hedged

- ISA Eligible

- Min Investment: £500 directly from Vanguard, £100 minimum for monthly direct debit. Min varies on other brokerage platforms

- Where To Buy: Vanguard UK or most trading platforms

** For full disclosure, I no longer own this bond fund as I decided to invest in 100% equities (shares) in early 2021. This is a risky move since equity markets can be volatile. **

The Vanguard Global Bond Index Fund is #2 on my best tracker funds list because the fees are low and the fund invests in thousands of international government and corporate bonds. It’s a great fund for bond diversification if you are considering bonds.

Understand that bond funds have their critics as you won’t make great returns during low-interest rate periods, plus bond funds are more boring than your grandma’s knitting lessons. But you usually won’t experience large value losses in your bond funds during a stock market correction, like the one in March 2020.

Bond funds are a tricky one. During higher interest periods, bond funds yields more but the bond prices fall and vice versa when interest rates rise. The dilemma is, you could just take your cash and put it into a fixed rate bank or government savings bond with zero risk and zero volatility but you won’t benefit when interest rates are low.

There are many investors who still stick buy the method of investing in equity trackers and balancing with bond trackers based on their age to hedge risk. For example, a 40 year old would allocate 60% to equities and 40% to bonds while a 70 year old would allocate 30% to equities and 70% to bonds.

What are the advantages? With fixed rate bonds you have to move your money around when the bonds matures. No problem if you are buying long duration bonds but most people take one or two year bonds and often times people forget when they mature and these bonds automatically renew at lower rates. Then money is locked away unless you take a penalty for withdrawal.

With the Vanguard Global Bond Index Fund, you don’t have to worry about this. You just set and forget. The problem is you might now receive the returns you would on a fixed rate bond. For example, from November 2022 to July 2023, the Vanguard Global Bond Index Fund hasn’t moved in price at all.

So what’s the point in owning a bond fund if they aren’t performing well?

Well if I were in my 20’s or 30’s I wouldn’t own any bond funds because at those ages, you have decades to recover from stock market volatility and corrections, but if you are older and approaching or in retirement, you might consider diversifying into bonds to protect your capital.

I sometimes own bond funds because they can act as an insurance policy and a hedge against stock market corrections such as the one in 2009.

If you owned a bond fund during market corrections, you will understand the benefits.

For example, the U.S. equivalent Vanguard Total Bond Fund gained 3.45% during the 2008-09 market crash while most managed equity funds lost 45%. When markets are falling, you can exchange some of your bond fund holdings into stock funds when the worst is over. Think of bond funds like insurance, you hope you won’t need them but you’ll be glad you have them when the markets are falling out of the sky.

(Please be aware however that bond funds are not immune from losses. From Jan 1st 2022 to Oct 31st 2022, my go to bond fund dropped from £162.27 to £138.61 which was a 14.5% loss.)

It’s important to understand bond index trackers can still fluctuate in price depending on interest rates but the fluctuations shouldn’t be so volatile. From June 1st, 2019 to May 31st, 2020, this bond fund returned 5.8%.

When interest rates increased, I moved away from bond funds into equities and FSCS backed savings accounts. In 2025, I’ve been considering moving back into bond funds as interest rate cuts look likely. If your risk tolerance is lower, you can use bond funds to balance out your portfolio.

So why not a UK bond fund?

A UK Government bond fund is higher risk than a global fund because it is far less diverse. For example, Vanguard’s UK Government Bond Fund only holds 58 bonds versus the 10,000+ bonds in the Global Fund.

Here are the return comparisons of both funds launched in 2009:

You can see over the last 10 years, the UK bond fund has underperfromed the Global Bond Fund, sometimes by a large amount (1 year yikes). The Government Bond UK fund is now rated at risk 5/7, the equity tracker is rated by Vanguard as 6/7.

If you still feel you want to hold some more UK bonds, a mix of the Global Bond and UK Bond funds would be a good solution.

I personally don’t hold any UK Government bond index tracker funds.

Why Vanguard or Fidelity?

Customers have entrusted over $5+ trillion to Vanguard making them one of the largest fund companies in the world. Aside from Vanguard’s stability and reputation, company founder Jack Bogle was the man responsible for launching the very first index tracker fund back in the 1970’s.

Vanguard & Fidelity has a long history of low-cost investing. Other companies offer low fees as an introductory rate, then quietly hike their fees. If you do invest in a company other than Vanguard, pick the companies with the lowest fees as most offer identical products.

A small percentage in extra fees can cost you lots of money over periods of time so pay close attention to fees. There are other companies that offer index trackers, just check the fees.

If you want to open a joint or corporate account, Vanguard doesn’t offer these so Fidelity would be a good solution. Fidelity offers joint accounts for up to three people.

Best way to buy trackers

Investengine: Zero fees using DIY portfolios. You just pay the fund fees. This is my favourite lowest cost method of buying funds. Click here to receive £100+ in Welcome Bonuses.

Vanguard: £500 minimum on each fund, £100 minimum for monthly direct debit and you can purchase any amount manually after you initial £500 purchase.

Fidelity: £25 minimum on each fund then you can purchase any amount after your initial deposit.

Etorro: You can buy stocks with 0% commissions. (Click this link to sign up).

Trading 212: £1 minimum deposit, you can buy ETF’s instead of the trackers. Trading 212 does have some currency exchange fees if you’re buying ETFs domiciled outside the UK. Thankfully the Vanguard S&P500 ETF is domiciled within the UK so you won’t pay any currency fees.

Stake: £1 minimum deposit, you can buy ETF’s instead of the trackers (Click this link to receive a bonus).

You can invest directly with Vanguard but each fund has a £500 minimum initial purchase. If you want to purchase less than £500 in each fund to start, I’d recommend opening an account with Fidelity where you can purchase the Fidelity Index US Fund which is similar to Vanguard’s version and only has a £25 minimum.

If you don’t want to use Fidelity, I’d recommend Investengine using their DIY portfolio option which has zero fees. I used to use Iweb because each trade is only £5 but now Etoro and Trading 212 offers free trades (aside of FX fees). After you reach the £500 fund minimums it’s more cost-effective to transfer to Vanguard if your current trading platform doesn’t charge you transfer fees.

If you have to buy through a brokerage platform, a discount broker will save you lots of money over the long run because you can avoid annual platform fees. For example, Charles Stanley charges an annual 0.25% platform fee (balances under £250,000) which really adds up over the years even though it doesn’t sound like much.

If you don’t trade often and your account balance is under £80,000, you’re better off investing directly through Vanguard since their annual account fee is only 0.15% (you can read more about this here). Low fees are crucial to successful long-term investing.

You can also buy trackers in the form of ETF’s or Exchange Traded Funds on Investengine or Trading 212.

So that’s how I recommend most people invest in the stock market; easy index tracker funds and finished.

Here’s a walkthrough video tutorial of how to purchase index trackers on Vanguard’s platform.

How much to invest?

So how do you decide how much to put into each type of the best index trackers? Stock tracker funds can be much riskier and more volatile than certain bond tracker funds but the payoff is greater. For example, here’s how Vanguard’s stock tracker and bond trackers performed during the financial crisis between May 2008 and May 2009 (I used the US equivalent funds as the Vanguard UK funds didn’t exist at the time):

| Fund | Performance |

| Vanguard Total Stock Market (VTSAX) | -36.10% |

| Vanguard Total Bond Market (VBMFX) | -1.17% |

As you can see the stock index fund suffered far worse losses than the bond fund. A stock tracker fund will fall as much as the entire market falls whereas a bond fund tends to be less volatile.

The way to decide what allocation works for you is to think about risk tolerance and this is different for everyone.

Some methods suggest taking your age and using that for the percentage of bond funds you should own.

Example: A 35 year-old would own 65% stock index funds and 35% bond index funds. You can adjust that based on your risk tolerance. I’m in my mid 40’s and own about 35% in bond funds. As you get older you can adjust this as needed (we call this rebalancing). A 20 to 30-year-old can afford to take more risk since they have time to rebound if disaster strikes, so their portfolio might be 90% stocks and 10% bonds.

Another method suggests age minus 10 or 20. It’s really up to you. The best to decide is calculate how much risk you are willing to take during a stock market correction and then allocatr from there.

Personally, my allocation when I owned bonds was somewhere in the 70-80% stocks and 20-30% bonds. Now my allocation is 60% equities and 40% in 1 year bonds and money market funds.

When considering bond trackers, I avoid strictly corporate bond funds as these bonds are debt held against private companies and don’t pay high enough returns to warrant the extra risk of company failure. The global bond fund I use has a high mix of government and a lower mix of corporate bonds.

Conclusion

Consider kissing those risky single stock portfolios goodbye and buying and holding the best tracker funds. This strategy provides less risk, less emotional stress and lower fees and is a very effective way to achieve retirement wealth. Even the greatest investor in the world, Warren Buffet, agrees:

“The trick is not to pick the right company, the trick is to essentially buy all the big companies through the S&P 500 (or index tracker fund) and to do it consistently and to do it in a very, very low cost waY”

Warren Buffet

CNBC Interview May 2017

This article highlights why index trackers are a great investing solution that has been time-tested. Take time to research the trackers as there are many offered by many different companies. Make sure you pay attention to what the trackers hold in their portfolios and the fees. As always, you should never invest in anything you don’t understand.

I love feedback, so if you find any errors or omissions or have any website improvement suggestions, I invite you to contact me and be a part of contributing to this website.

Disclaimer: This page is for information purposes only. This information is not financial advice and has been prepared without taking your objectives, financial situation or needs into account. You should consider its appropriateness for your circumstances. All investing carries risks. Opinions expressed in this review are opinions based on my own personal experiences. The FSCS does not cover index trackers or peer to peer lending and your capital is at risk. Please don’t invest more than you can afford to lose.